TODAY UMNO HAS PROVEN ITSELF AS A PARIAH PARTY WITH A PARIAH LEADER.

ISAKI – Excellent Japanese Food & Wonderful Ambience

Isaki or Grunt Fish has a very light and delicate taste. Grunt fish can be eaten as sashimi, grilled with salt or marinated with chili leaves. Isaki is also a wonderful restaurant in Sri Hartamas. Located at the end of the row that houses Backyard pub, Bulldog, Aunty Nat and Saigon .

I love its outdoor garden setting. Coming into the open bench area that is its portico, one gets a nice feeling to the place, a friendly vibe that Isaki has a casual dining side to it. The pebble lined walk, the Japanese wooden lanterns and small pine wood slats that the waitresses scurry across in typical wooden sandals. Upstairs is a large area that lends itself perfectly to parties and events, with ample bar and seating. You get the overall impression of intimacy and minimal pretensions here. Here I have to say that they make the best sushi rice – an often overlooked factor. I mean, the seafood has to be fresh and the cuts appropriate, those are a given. However, not many places take the case to come up with proper sushi rice. I shy away from the Sushi Kings and Sakae Sushis because they have no idea how to do the sushi rice. Maybe its because they are “process-manufactured”, the rice is packed as hard as a chinese dumpling, and the rice vinegar-sugar-water-salt mix is almost indistinguishable. In Isaki’s case, the mix is excellent plus I suspect they do put in a dash of sake or kombu.

Isaki’s sushi rice is so good, I can eat the rice on its own.

Somehow, a good sushi rice place has to equate to a good place for sake. At Isaki, you know they are serious when they have 4 different huge sake bottles being heated at any one time, and the sake menu is extensive.

I have never seen a Japanese restaurant that has so many pork items on their menu – its an eye opener. It could very well be that the restaurant is more influenced by Okinawan cooking (will ask them next time). Okinawan cooking tends toward stronger and spicier flavors than Japanese food, and is more heavily influenced by Chinese cooking styles. Hence pork is a very important ingredient to Okinawan cooking. Other items on the menu that are very good: the buta kakuni (steamed pork belly) and buta shishilo itame (pork slices with Japanese chillies). The garden setting makes for a wonderful place to have a barbecue as well, as almost one-third of their menu is catered to having the mini barbecue pit at your table. Fresh ingredients, lotsa meats and veggies, lotsa sake (hot and cold), wonderful outdoor setting, how not to like the place.

I have never seen a Japanese restaurant that has so many pork items on their menu – its an eye opener. It could very well be that the restaurant is more influenced by Okinawan cooking (will ask them next time). Okinawan cooking tends toward stronger and spicier flavors than Japanese food, and is more heavily influenced by Chinese cooking styles. Hence pork is a very important ingredient to Okinawan cooking. Other items on the menu that are very good: the buta kakuni (steamed pork belly) and buta shishilo itame (pork slices with Japanese chillies). The garden setting makes for a wonderful place to have a barbecue as well, as almost one-third of their menu is catered to having the mini barbecue pit at your table. Fresh ingredients, lotsa meats and veggies, lotsa sake (hot and cold), wonderful outdoor setting, how not to like the place.

Lastly, I want to mention that its a very dog friendly place. If you go in the evening, you are likely to see the owners, a tanned Japanese man who won’t be back in Japan anytime soon and a lovely Chemor girl called Maggie Liew, with their two beautiful dogs – one is the cutest bulldog that looks like a bodybuilder gone bad, while the other is a lovely dobbiemix with a nice shiny coat – both absolutely people friendly. The place is very dog friendly.

I know some people has a list of so called pet friendly eateries – to me, most of them are not pet friendly, but rather if they have a patio/verandah, they don’t mind you bringing your pets. Those are pets tolerant places, not pet friendly, they just accomodate you because of your business. Genuine pet friendly places are an inclusive and embracing environment for responsible dog owners who bring their dogs out because they are part of their family rather than just pets.

I know some people has a list of so called pet friendly eateries – to me, most of them are not pet friendly, but rather if they have a patio/verandah, they don’t mind you bringing your pets. Those are pets tolerant places, not pet friendly, they just accomodate you because of your business. Genuine pet friendly places are an inclusive and embracing environment for responsible dog owners who bring their dogs out because they are part of their family rather than just pets.

EPF Should Not Sell PLUS

Is there an alternative to North South Highway? How much of toll roads come under PLUS? There are 14.5m EPF members. We begrudgingly pay tolls, at least thinking some of it goes back to EPF returns.

If you look at our population bell curve, you can surmise that we are a growing population with a relatively wider base. In many aspects we are skewed towards a younger working population. This means that the annual contributions to EPF is likely to grow even more.

We can also surmise that there are limited investing opportunities locally, taking into account the kind of risk EPF is allowed to partake. PLUS is a significant player in an infrastructure that plays a critical role for the country. To replace PLUS with a similar investment with similar returns would be very difficult.

Fair Value – Not Enough Even

As a socialist-capitalist, I can be torn between getting more than a fair return on investment. That is, if an asset is being sold at higher than normal valuations, by all means, sell. I am certain that any potential buyer would have to offer a premium. The question then is how much of a premium would it make sense for EPF and Khazanah to dispose PLUS.

To me, the premium would have to be very high, so high that it would be silly not to sell, so high that it would be sillier to buy.

p/s: Yoona of Girls Generation

Critical Asset

Imagine a few years down the road, instead of the usual 5-10% annual increment, you see your normal RM1.10 toll

being raised to RM2.50. I am not saying it will happen. Yes there are rules to safeguard some of the increments, but seriously, it can only go up, and it won’t be LESS than when EPF/Khazanah are the owners.

We are already having to increase our investing overseas owing to the deluge of contributions into EPF. We should not replace PLUS or assets with similar values.

Cornerstones Should Not Be Tampered With

We should be thankful that EPF has been able to give around 6% annual returns (tax free). Go and ask CPF whats their rate for the past few years. The high-ish rate is thanks to a solid platform girding the overall investing philosophy. Cagamas and other critical asset like PLUS are the cornerstones. You do not want to remove the cornerstones as the foundation would be shaky then.

Bull Bear Major Indicators

(Farah Ann Abdul Hadi)

There are tons of financial newsletters but the only one I read religiously is Maudlin Economics. His views are fair, mostly objective, minimal emotional attachment and logical. One of his recent articles entered on whether the bull run globally is over. ET To Elliot …

ET To Elliot …

The Elliott Wave Principle, all the rage in the 1980s, is less influential now but is still watched by the technical analysis team at Goldman Sachs. The Elliott Wave comprises sequential upward and downward market moves – “waves” – that form repeating cycles. A full cycle has eight waves. Waves 1–5 are bullish, with only minor pullbacks between. Waves 6–8 are corrective, or bearish, and you do not want to be long when they happen.

The market is presently in wave 4, according to Goldman market technician Sheba Jafari. That means the next downturn will be limited and followed by another bullish wave. Then we would see a bigger correction.

200 Day Moving Average

The 200 day MA is not a very solid indicator but as a guide to overall trend it gives you a lot of flags to be turn cautious. No point looking at Dow Jones index as the composition consists of too few stocks. Hence in order of importance, look at the S&P 500, the NASDAQ, Dow Jones and the Russell 2000. The first three are all above their 200-day moving average, and the Russell just dipped below its 200-day average.

Russell 2000 are the broadest in coverage and might have more retail attention and a lot less institutional interest. The bulk of the market is “controlled” by big funds’ movements and not retail.

Hence when the more important indices start to break 200 day MA on the way down, its a red flag to be cautious.

Corporate Earnings

When you buy a stock, you are really buying its future earnings: Each share’s price is the discounted present value of its expected future earnings. Prices change when expectations change, which happens for many different reasons.

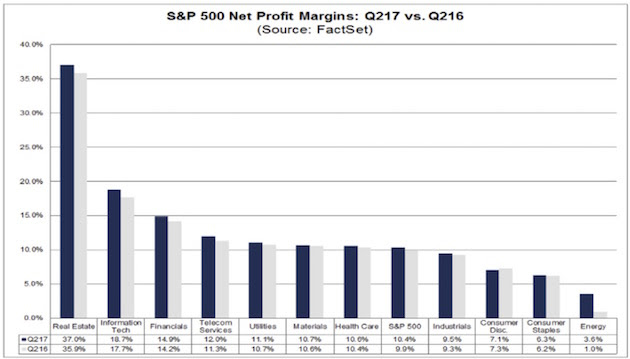

The present bull market is still with us in large part because earnings are pretty good. With most of the second-quarter reports now in, FactSet reported in its August 11th letter a 10.2% blended S&P 500 earnings growth since the same period in 2016. Earnings grew in every sector except Consumer Discretionary.

Factors To Watch

The global bull run will continue to edge ahead as long as the following are intact, according to Maudlin Economics, and I agree:

1. Global growth would have had to decelerate. It is not.

(European growth is actually picking up. Germany blinked on financing Italian bank debt, and the markets now have more confidence that Draghi can do whatever it takes.)

2. Wages and inflation would have had to rise. They are not.

3. The Fed would have planned to tighten monetary policy significantly. It is not.

(They should have been raising rates four years ago. It is too late in the cycle now. They may raise rates once more, but the paltry amount of “quantitative tightening” they are likely to do is not going to amount to much.)

(They should have been raising rates four years ago. It is too late in the cycle now. They may raise rates once more, but the paltry amount of “quantitative tightening” they are likely to do is not going to amount to much.)4. The ECB would have to tighten policy substantially. It will likely not.

(Draghi will go through the motions, though he knows he is limited in what he can actually do – unless for some unexpected reason Europe takes off to the upside. And while Eastern Europe is actually doing that, “Old Europe” is not.)

5. Credit growth would have had to be surging. It is not.

(Credit growth is generally picking up but not surging. And most of the credit growth is in government debt.)

6. Equities would have had to be expensive relative to bonds. They are not.

7. Investors would have had to be euphoric about equities. They are not.

8. High-yield spreads would have had to be widening. They are not.

(I pay attention to high-yield spreads, a classic warning sign of a turn in market behavior. Are they at dangerous levels? Damn, Skippy, I cannot believe some of the bonds that are being sold out in the marketplace. Not that I can’t believe the sellers are willing to take the money – you’d have to be an idiot not to take free money with no strings attached. I just don’t understand why major institutions are buying this nonsense.)

9. The classic signs of excess would have had to be evident. They are not.

10. China’s credit binge would have had to threaten the global financial system. It does not.

(Xi has somehow managed to push off the credit crisis, at least for the rest of this year, until after the five-year Congress. Rather amazing.)

11. Global trade would have had to be weakening. It is not.

12. The US dollar would have had to be strengthening. It is not.

Conclusion

The longevity of the current global bull run has a lot more to do with the massive quant easing taken after the 2008 financial crisis. It has plugged many holes, but almost every central bank has NOT done anything to rein in the excess liquidity. While growth is evident over the last couple of years, the recovery is still very ginger in the most affected countries. No central bank is willing to tempt fate by pulling back the liquidity.

As long as that persists, interest rates environment will still be very low in the affected countries. That will play itself out into the various financial assets and instruments, making for a very “low risk” environment favouring equities.

9am Lowdown: Toshiba – accounting scandal causes further woes

Good morning. Here is this morning’s news.

Toshiba: Accounting scandal causes further woes

Toshiba looks set to cut 7000 jobs after making a record loss of $4.53bn after their $1.3bn accounting scandal.

This news ends a woeful year for the accounting scandal-hit electronic giant. The revelations led to the resignation of Toshiba president and vice president. The BBC has reports that Toshiba’s shares have lost about 40% of its value since news of the profit overstatement began to emerge in April.

Tosbia said in a statement: “By implementing this plan, we would like to regain the trust of all stakeholders including shareholders and transform ourselves into a robust business.”

Cosmetic tax fraudster

Download our guide

How to break MTD into manageable steps

A beauty product trader has been jailed after an HMRC investigation which found she had stolen £750,000 in VAT by tampering with paperwork she could increase her repayment claims.

Chyi Chiann Cheah was caught after HMRC officers found she had vanished to escape investigation. Over a ten year period, she produced and submitted false invoices and shipping documents to support her claims for VAT repayments

Paul Barton, Assistant Director, Fraud Investigation Service, HMRC said:“Cheah thought she could hide from HMRC and avoid the consequences of her fraud. She was wrong. She cheated the taxpayer out of hundreds of thousands of pounds which should have been spent on essential public services and is now paying the price as she starts her jail term.”

Community: Anyone considered franchising?

Atkinson accountancy asked the AccountingWEB community whether they have had any dealings with the cheapaccounting franchise, and if so, how they found them.

Franchises fills Monnbeam with dread: “I’ve heard of lots of horror stories of other franchisees and I just get that claustrophobic feeling that you pay all that money and things don’t work out the way you were led to believe they would.”

CheekyChappy agrees: “I would feel that I wouldn’t have the freedom I do now, and I would also have to pay extortionate fees for things I could do myself for much less.”

Has anyone had any success signing up as a franchise?