Next week on 26th April, PUC will be holding its EGM to approve the acquisition of a 33% stake in Pictureworks, which comes with guaranteed profits for two years. PUC sprang a surprise just prior to the important EGM by disclosing the deal with 11th Street. In one fell swoop, we basically have the largest listed internet commerce entity in Malaysia.

Can anybody say that internet commerce will not grow even more significantly in Malaysia over the next 2, 5, 10 years? Well, how can anyone “participate” in that growth in a listed vehicle? Now you have it.

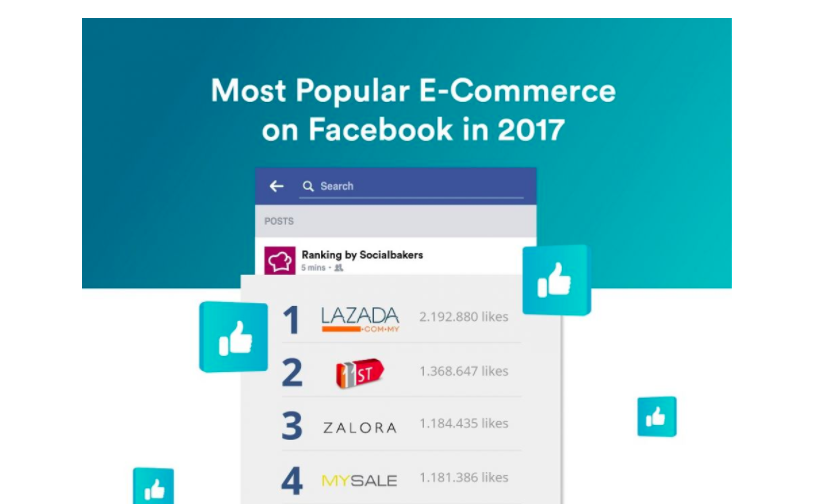

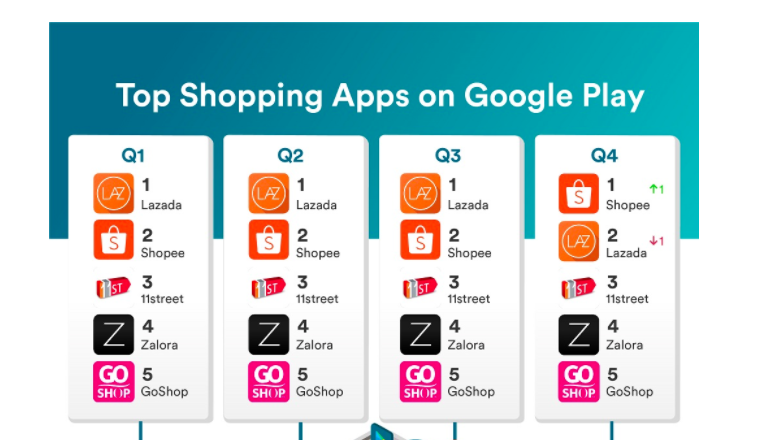

Ask yourself, can you buy a stake in Lazada or Shopee or even Zalora??? Yes, maybe when they actually list. Plus when they do, you can be sure the valuations will be astronomical (in the billions of USD).

Lazada, is backed by Ant Financial and Alibaba. Enough said.

Shopee is backed by Garena Group. Garena is backed by Tencent.

Celcom Planet Sdn Bhd is a joint venture between ADS and SKP, which owns and operates an e-commerce platform known as 11Street Malaysia, and is one of the largest e-commerce companies established in Malaysia. 11Street Malaysia was originally a leading e-commerce company in South Korea, operating under the management of SK Planet Co., Ltd. which expanded its operations to Malaysia to grow and expand the e-commerce industry in the country. From 2015 to 2017, 11Street Malaysia reported an achievement of more than 300% growth in gross merchandising value (“GMV”), 160% growth to over 13 million product listings, and 200% increase to 40,000 sellers registered on its platform. As of 31 December 2017, 11Street Malaysia recorded a GMV of approximately RM427million for financial ended 31 December 2017, and total monthly unique visitors (“UV”) of 13.5million for the month of December 2017.

The Investment Amount translates to an implied valuation of 100% equity interest in CPSB ranging from MYR333.33 million to MYR375.00 million (the “Implied Valuation”).

How expensive was the deal? If you were to take the historical Gross Merchandising Value of RM450m, it means PUC is coming in at a staggeringly cheap P/GMV of 0.6x. How cheap is that? Well, similar deals in the same tech sector have been in the 1.5-2.0x.

Why would Axiata/Celcom do such a deal? One, that the management of PUC has the ability and vision to take 11th Street to the next level. If you look at the new ownership structure, the original shareholders will still hold much hight stakes than PUC in 11th Street, so nobody’s cashing out.

I believe some of the RM90m will be used to pay down debt at 11th Street. The burn rate at 11th Street has passed the initial setup stage. They are recording good growth and good revenues, hence any synergies and cost savings will go swiftly to the bottom line.

PUC shall be appointed as a preferred partner of 11Street Malaysia provided that it shall offer competitive terms to 11Street Malaysia for the following (“Synergistic Collaboration”):- a. 11Street Malaysia’s marketing needs, especially in digital marketing; b. 11Street Malaysia’s payment gateway requirements for all its eCommerce services with PUC’s flagship digital services platform (“Presto”) being nominated and implemented as the Company’s preferred payment platform on all of its eCommerce services; and c. 11Street Malaysia’s technology needs for its eCommerce infrastructure and platform.

This is key to the transaction, elevation of PUC as the management and preferred partner. Obvious immediate synergies in e-marketing and e-advertising, the usual rice bowls for PUC. The management of PUC will be directing and putting in place the future direction of 11th Street, which is critical in being part of a listed entity.

PUC wishes to announce that the Company had on 12 April 2018 incorporated a wholly-owned subsidiary in Malaysia, namely PUC Ventures Sdn Bhd (“PVSB”), under the Malaysian Companies Act 2016 (“Incorporation”). PVSB is incorporated as an investment holding with an initial issued share capital of RM1.00 comprising one (1) ordinary share. It is intended that PVSB identifies opportunities to invest or acquire equity interests in and/or enter into strategic alliances / joint-ventures with companies which are principally involved in electronic commerce (“e-Commerce”) businesses, electronic payment services, financial services, technological services, and related businesses including but not limited to media services, airline and accommodation services related (“Target Segments”), which are synergistic and complementary to the existing businesses of PUC and its subsidiaries.

This announcement which came last week would actually be quite significant. The establishment of PUC Ventures would indicate that Pictureworks and 11th Street and e-Wallet and Presto etc… would not be just a mish mash of investments by PUC. It speaks of a bigger cohesive agenda by PUC going forward. I believe PUC is mapping itself as a smaller Meituan or Tencent.

CONCLUSION

a) Valuation wise – PUC looks particularly compelling – just taking into account the impending absorption of the proposed stake in Pictureworks, which is very undemanding. Added to the guaranteed profit for two years, Pictureworks has a very good chance to be listed in HKSE Gem, which will translate to a substantive “potential value unlocking” if/when Pictureworks lists. Just follow the steady roster of clientele of Pictureworks: Malaysia, HK, China, Singapore… but largely in China, which bodes well for a China/HK listing (comfort level based on source/location of revenues).

b) Valuation wise – As indicated above, the P/GMV for the 11th Street deal makes a lot of sense for PUC. Should they be able to bring up the revenues of 11th Street from 2017’s RM427m to a billion ringgit within 2-4 years, that would certainly make it highly attractive to list or be sold to even bigger whales at a valuation closer to 2.0x P/GMV. As always, 11th Street is a highly sought after asset platform, hence the permutations for a sale or joint venture or seperate listing are always on the table. Another potential kicker in PUC’s inherent value, which they bought at a very reasonable valuation.

c) A COUP – If you were to believe the media, JD.com and Alibaba were also trying hard to buy 11th Street. Of course both have bigger firepower and money, but then it would immediately lose its Malaysian roots. I think thats part of the broader strategy by Axiata/Celcom, to bring in a local champion and bring about much higher valuation, maybe a Malaysian “unicorn” in the making.

https://www.lowyat.net/2017/143327/report-alibaba-jd-com-competing-acquire-11street-malaysia/

d) Institutional Funds – Fund managers now can no longer ignore PUC. It is a “must have” being the biggest listed internet commerce entity. That should see an upsurge in institutional holders.

e) Data Science & A.I. – The bigger picture going forward. I think PUC is one of the very very few tech based companies that understand the whole ecosystem of the new world and the new future. PUC Ventures would be the vehicle to jumpstart alliances and investments. Just gauging its corporate moves for the past years and a half would paint a company and leadership that understands the really “big picture”.