How many more times does Anwar need to be stabbed?

Trust is not a worthy word given that family and close friends play each other out for financial gain or for power etc.

Everybody encounter it once or couple of times in their life.

But Anwar has the worst encounter not once but twice.

And the person who helped make this happens is Azmin.

Azmin has always being grateful to Mahathir for giving financial assistance to study, work and now a beautiful standing as Minister in Economic which he knows nuts.

So with the backing of Mahathir and Daim with fund of US16.91 billion which was stolen and transferred out of Malaysia recently what has Azmin Ali got to lose.

Win or lose, Mahathir is still the PM and his position as Minister is secure while the money is there to swim in.

AZMIN ALI IS DEFINITELY GOING TO CHALLENGE DSAI FOR THE TOP POST IN PKR.

Who is the Jinx?

Within 100 days already there are two death.

Sungei Kandis and now Balakong.

In Chinese it is bad omen.

So who is the jinx?

Mahathir or Amirudin Shaari?

Does this has something to do with the paper loss of US$1.91 BILLION but in reality it was real money of US$16.91 BILLION transferred out of Malaysia?

Is Allah giving more signs?

That’s Not The Way Share Market Works

Encik Shahril of Sapura Energy had to defend his total take-home package of around RM70m a year for the past few years. Specifically since FY 2014.

His defense was that there was a covenant. If he won’t sell his shares, the company would get better interest rates on loans. Seemingly to imply that some major lenders will only lend to Sapura Energy only if he stayed.

Errr, that’s not the way a share market works. The remuneration committee cannot and should not take into account whatever “covenant” with lenders intimated with the CEO. It is like saying I am the CEO and I had to sell my mother’s house so that I don’t have to sell my shares in the company, so that share price doesn’t collapse and the lenders only wanted to deal with me as CEO. That’s not the way a share market works… I think.

Are you telling me that all 1,000 banks in Asia would not lend to you unless you stay as CEO and do not sell your shares? Even if that was the case, was the RM50-80m a year from FY2014 to compensate you for “opportunity cost” and “losses”? Who compensates the minority shareholders’ losses???? That’s not the way sharemarket works.

The remuneration committee can choose to reward the CEO if there had been reasonable stretch targets met, or even positioning the company to meet future challenges. The bottom line is that whatever you reward the CEO must have been to the benefit of ALL SHAREHOLDERS, either in new earnings achieved or price appreciation. There has been none of that.

You can try to argue that the CEO has positioned the company to face the new market conditions and restrategize the company’s direction over the last few years. Hence all shareholders will benefit from that. Again, while that is all good, IT MUST BE REFLECTED IN EARNINGS and PRICE APPRECIATION. If the positioning is so good for long term, then give la bonus WHEN these long-term strategies pan out. NOT BEFORE THAT.

The market cap of Sapura Energy has been between RM3.3bn to RM4.5bn over the last 12 months. At RM80m a year, that means the CEO gets approximately 1% to 2% of total market cap of the company a year. If the company continues to lose money, or even break even for 10 years… it means the CEO would have gotten between 10% to 20% of the market cap of the company for not doing terribly well.

Mind you Encik Shahril owns just 16%, which translates to a value of RM520m to RM720m. Now put that in perspective, RM70m-RM80m in compensation a year is a bit much.

That’s certainly not how the share market works. I think.

(above is a copy of the remuneration framework of a good listed company … in this case, it was Apple Inc.)

It is not just at Sapura Energy. Just go and examine the total board compensation, in particular to the CEO, of the following companies. The board remuneration is totally out of whack with whatever business metrics you want to use to measure good or great performance:

Genting

KNM

Salcon

Maybank

IHH Healthcare

IOI

Maxis

TA Enterprise

YTL

There are those who are owner controlled, which makes it difficult when they pay themselves an over the top amount. You already owned a controlling stake, if you perform well, your equity will rise. Be like Li Ka Shing, he pays himself HK5,000 dollar a year as compensation.

Asset Class Returns In The USA

The brilliant snapshot of asset class returns compiled by Blackrock makes for interesting analysis. See if you can deduce any pointers from the table. 100 persons could be looking at the same table and arrive at differing conclusions.

To develop a keen interest in investing is the continue to develop your ability to link and see cause-and-effects from seemingly disparate factors.

a) Look at 2008 when the financial crisis impacted. When all hell breaks loose, does it matter what kind of stocks you were in? Well, long and short answer, NO. Large caps core -37%, Large caps growth -38.4%, Large caps value -36.9%, Small caps -33.8%. There’s no place to hide apparently. But when big boss sneezes, the rest of the world catches a worse cold, EVEN THOUGH IT WASN’T BLOODY OUR FAULT!!! International stocks were down -43.4%. Where is the justification?

b) The following years till 2017 were all UP years, thanks to the relentless printing of money by the Federal Reserve and EU. The exception was 2011 where equities had a terrible year. When the US had a terrible year you can bet that international equities would have an even worse year. Large cap growth 2.6%, Large cap core 2.1%, Large cap value 0.4%, Small caps -4.2%… and international equities ta-dah -12.1%.

c) For those risk-averse players selecting dividend stocks, well, they performed as expected in a normal market. But when crisis hits like in 2008, it was also down -22.8%. In the difficult 2011 dividend stocks only eked out a 1.8% return.

d) Two down years out of 11 is not that bad, but it also points to the conclusion that we are ripe for another DOWN/CRISIS year soon. It comes around like clockwork because markets never forget and investors always forget, and you can quote me on this.

e) Just look at the last 5 years, these equity asset classes are just taking their sweet rotational play year in year out thanks to low-interest rates and excess liquidity due to the flagrant printing of money. There’s nothing academic about it, just kids playing with an increasing number of toys.

… we are ripe for another DOWN/CRISIS year soon. It comes around like clockwork because markets never forget and investors always forget …

Catch These Movies: THE LEAKERS & BROTHER OF THE YEAR

The Leakers – Helmed by the often brilliant Herman Yau Nai Hoi (whom I believe was from Malaysia who became a great success in HK films). 70% of the movie was shot in Georgetown.

The Leakers – Helmed by the often brilliant Herman Yau Nai Hoi (whom I believe was from Malaysia who became a great success in HK films). 70% of the movie was shot in Georgetown.

Good story, good plot twists galore, non-stop action, even the two car chases in Penang were pretty well done. Good acting from the top 4 cast members: Julian Cheung, Charmaine Sheh, Francis Ng and Kent Cheng.

Two sons of a Malaysian pharmaceutical owner went against their father’s business practices. Reliving SARs all over again somewhat. Part Mission Impossible, put in two cops – one straight as an arrow, the other to solve crimes at all cost. Non stop action. 90/100

Brother of The Year – The Thais continue to win more Asian viewers with their non-horror genre such as Bad Genius and this comedy feature. Kind of simple story but good storyline and acting, in particular towards the last 1/3 of the movie, managed to dissect many dysfunctional brother-sister relationships. 88/100

The Tide Has Turned?

The local bourse has been drifting down for weeks now with no respite in sight. As written a few weeks back, Malaysia’s problems were not largely associated with the USA-China trade wars:

The Problems: We are in the midst of “house-cleaning”, while we are quite prepared to be patient, a few things are noteworthy.

a) Removing of GLC CEOs and other BN appointees from important government positions – While I wholeheartedly support this, it also hampers all these affected GLCs to “move” or carry out projects. Nobody dares to negotiate contracts as the situation at the top is still fluid. This has to be managed FAST and QUICK. The longer we carry out this bloodletting, the longer the downtrend of the market will be. There is a very low-velocity number in the current velocity of money.

b) Tainted Companies – Those not in the GLCs bracket but ‘tainted’ listed companies are affected as well. Quite a number of these company owners are currently hiding in overseas waiting for the dust to settle. When the owners are not around and their fate so uncertain, these companies will do as little as possible.

c) Clean Listed Companies – They may not need to hide but since nothing is moving at the government level, it also meant the wheels of economic activity also grinds to a halt.

Our PM and the Council of Elders must put in their strategy and action plan to work fast. More so when it comes to Malaysia because our country is highly dependent on the stock market as a major catalyst for domestic economic activity. Malaysia has one of the highest percentages of GDP that is listed on the stock market (over 75% by guesstimate) – that translates to a high correlation for market activity with the real economy.

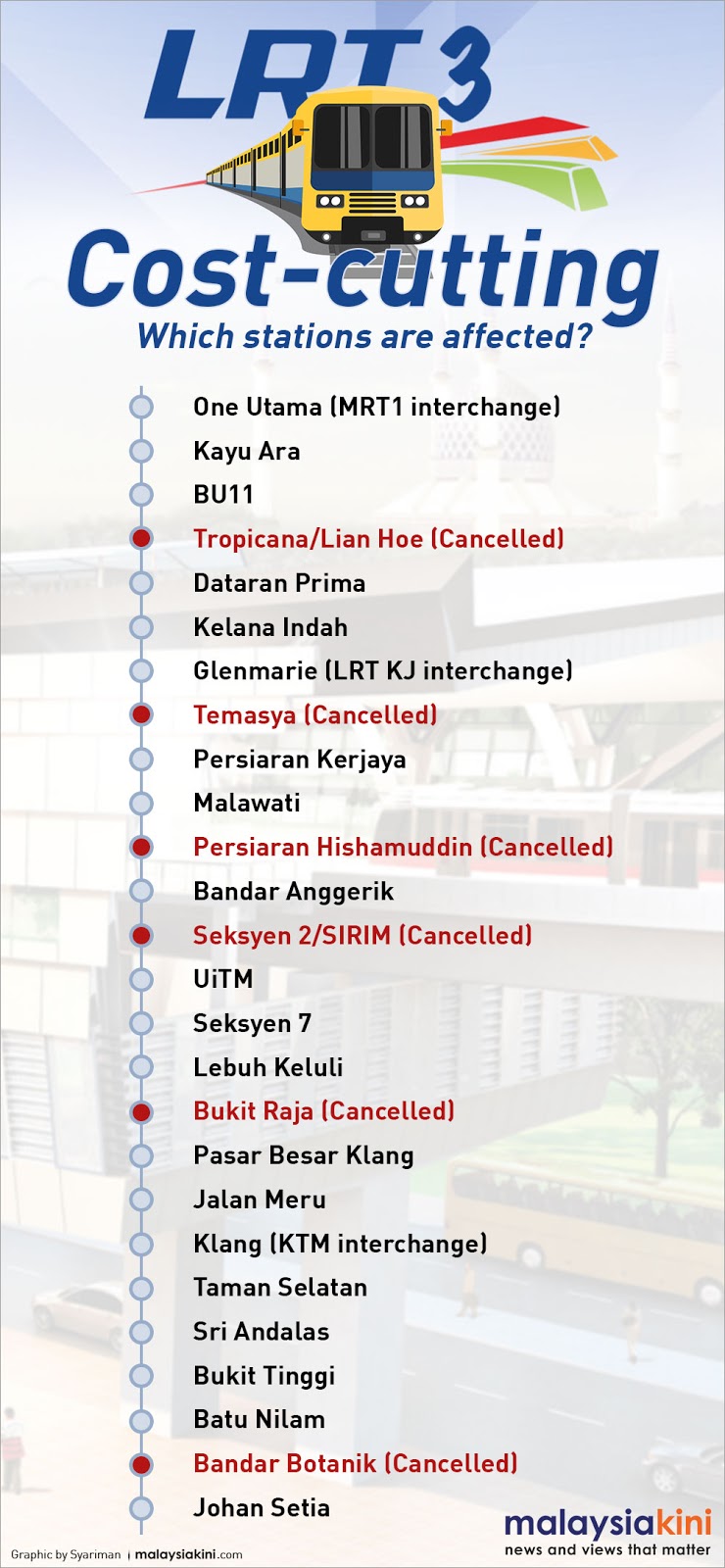

However, today saw some silver lining appearing when the Minister of Finance approves the go-ahead for LRT3 project.

http://www.theedgemarkets.com/article/george-kent-mrcb-after-lrt3-set-proceed

This was very significant as instead of removing people from GLCs, we are starting to green light projects. Things needed to move. This move, in particular, was more meaningful in other ways. This project basically helmed by two “friendly counters to Najib’s administration” (one more so than the other). It may be a signal that the bloodletting is over, now let’s move on. As long as you stay the course of proper business management with no impropriety, you can be part of New Malaysia. If that’s the message, its a huge relief for plenty of listed company owners.

TIMING

The timing couldn’t have come at a better time. Let’s look at the China trips coming up for Malaysia’s top guns:

a) Finance Minister will be going to China end of the month of July

b) Tun Daim will be going a few days before Lim Guan Eng

c) PM will be going to China mid August.

Last month, it was reported that Prime Minister Tun Dr Mahathir Mohamad had said Guan Eng and Malaysian Anti-Corruption Commission officers will travel to China soon to discuss with relevant officials about the two gas pipeline projects under SSER. Before that, Dr Mahathir had also noted the need to renegotiate unequal terms of the controversial ECRL project.

So why do we need 3 separate trips? One can only argue about it logically since I am not inside those meeting rooms.

My theory is that Tun Daim has to go earlier than LGE to meet with “the real big guns” behind the scenes with appointments set up by Robert Kuok. Why? Because the whole shebang with China needs to be concluded positively with no hiccups.

I expect Daim and Robert to meet with people who can work the overall strategic picture. I expect the two to voice the case for Malaysia, how we have turned a corner, how we now have to grapple with a significant level of government debt and liabilities, how China can use the situation to further clamp down on “corruption” by China state firms overseas, how both countries can come up smelling like roses …

China needs Malaysia in a way to consolidate ties in Southeast Asia, not just for the One Belt One Road thing but strategically China wants a partner to have indirect oversight over the Straits of Melaka, militarily and economically.

Only with the “heads up OK” from the real bigwigs can LGE go and renegotiate better terms for the existing China-linked contracts in Malaysia.

Hence when PM goes over, it will be a rapturous ceremony to seal the beginning of a new partnership. I see palm oil buying to be a major issue which can jump start Malaysia’s major industry. Closer ties and agreements with respect to foreign exchange and mutual “support” of each others’ currencies and its usage in trade could be forthcoming.

These potential developments are important as there are still plenty of genuine projects related to One Belt One Road for Malaysia and China. It will also mean that its not a “sin” to have a China company as partner in future projects.

The tide has finally turned?

Cautiously optimistic.

Read Romelu Lukaku’s Story

Besides supporting my good friend from Belgium … read Lukaku’s story (blood, sweat, tears and some more):

…He was like, “How old is this kid? Where is his I.D.? Where is he from?” I thought, Where am I from? What? I was born in Antwerp. I’m from Belgium.

I knew we were struggling. But when she was mixing in water with the milk, I realized it was over, you know what I mean? This was our life.

If you don’t like the way I play, that’s fine. But I was born here. I grew up in Antwerp, and Liège and Brussels. I dreamed of playing for Anderlecht. I dreamed of being Vincent Kompany. I’ll start a sentence in French and finish it in Dutch, and I’ll throw in some Spanish or Portuguese or Lingala, depending on what neighborhood we’re in.

I’m Belgian.

I’ve Got Some Things to Say

remember the exact moment I knew we were broke. I can still picture my mum at the refrigerator and the look on her face.

I was six years old, and I came home for lunch during our break at school. My mum had the same thing on the menu every single day: Bread and milk. When you’re a kid, you don’t even think about it. But I guess that’s what we could afford.

Then this one day I came home, and I walked into the kitchen, and I saw my mum at the refrigerator with the box of milk, like normal. But this time she was mixing something in with it. She was shaking it all up, you know? I didn’t understand what was going on. Then she brought my lunch over to me, and she was smiling like everything was cool. But I realized right away what was going on.

She was mixing water in with the milk. We didn’t have enough money to make it last the whole week. We were broke. Not just poor, but broke.

My father had been a pro footballer, but he was at the end of his career and the money was all gone. The first thing to go was the cable TV. No more football. No more Match of the Day. No signal.

Then I’d come home at night and the lights would be shut off. No electricity for two, three weeks at a time.

Then I’d want to take a bath, and there would be no hot water. My mum would heat up a kettle on the stove, and I’d stand in the shower splashing the warm water on top of my head with a cup.

There were even times when my mum had to “borrow” bread from the bakery down the street. The bakers knew me and my little brother, so they’d let her take a loaf of bread on Monday and pay them back on Friday.

I knew we were struggling. But when she was mixing in water with the milk, I realized it was over, you know what I mean? This was our life.

I didn’t say a word. I didn’t want her to stress. I just ate my lunch. But I swear to God, I made a promise to myself that day. It was like somebody snapped their fingers and woke me up. I knew exactly what I had to do, and what I was going to do.

I couldn’t see my mother living like that. Nah, nah, nah. I couldn’t have that.

People in football love to talk about mental strength. Well, I’m the strongest dude you’re ever going to meet. Because I remember sitting in the dark with my brother and my mom, saying our prayers, and thinking, believing, knowing … it’s going to happen.

I kept my promise to myself for a while. But then some days I’d come home from school and find my mum crying. So I finally told her one day, “Mum, it’s gonna change. You’ll see. I’m going to play football for Anderlecht, and it’s going to happen soon. We’ll be good. You won’t have to worry anymore.”

I was six.

I asked my father, “When can you start playing professional football?”

He said, “Sixteen.”

I said, “O.K., sixteen then.”

It was going to happen. Period.

Let me tell you something — every game I ever played was a Final. When I played in the park, it was a Final. When I played during break in kindergarten, it was a Final. I’m dead-ass serious. I used to try to tear the cover off the ball every time I shot it. Full power. We weren’t hitting R1, bro. No finesse shot. I didn’t have the new FIFA. I didn’t have a Playstation. I wasn’t playing around. I was trying to kill you.

When I started growing taller, some of the teachers and the parents would be stressing me. I’ll never forget the first time I heard one of the adults say, “Hey, how old are you? What year were you born?”

I’m like, What? Are you serious?

When I was 11 years old, I was playing for the Lièrse youth team, and one of the parents from the other team literally tried to stop me from going on the pitch. He was like, “How old is this kid? Where is his I.D.? Where is he from?”

I thought, Where am I from? What? I was born in Antwerp. I’m from Belgium.

My dad wasn’t there, because he didn’t have a car to drive to my away games. I was all alone, and I had to stand up for myself. I went and got my I.D. from my bag and showed it to all the parents, and they were passing it around inspecting it, and I remember the blood just rushing through me … and I thought, “Oh, I’m gonna kill your son even more now. I was already going to kill him, but now I’m gonna destroy him. You’re gonna drive the boy home crying now.”

I wanted to be the best footballer in Belgian history. That was my goal. Not good. Not great. The best. I played with so much anger, because of a lot of things … because of the rats running around in our apartment … because I couldn’t watch the Champions League … because of how the other parents used to look at me.

I was on a mission.

When I was 12, I scored 76 goals in 34 games.

I scored them all wearing my dad’s shoes. Once our feet got to be the same size, we used to share.

One day I called up my grandfather — my mum’s dad. He was one of the most important people in my life. He was my connection back to Congo, where my mum and dad are from. So I was on the phone with him one day, and I said, “Yeah, I’m doing really well. I scored 76 goals, and we won the league. The big teams are noticing me.”

And usually, he always wanted to hear about my football. But this time it was strange. He said, “Yeah, Rom. Yeah, that’s great. But can you do me a favor?”

I said, “Yeah, what is it?”

He said, “Can you look after my daughter, please?”

I remember being so confused. Like, what’s Grandad on about?

I said, “Mum? Yeah, we’re cool. We’re O.K.”

He said, “No, promise me. Can you promise me? Just look after my daughter. Just look after her for me, O.K.?”

I said, “Yeah, Granddad. I got it. I promise you.”

Five days later he passed away. And then I understood what he really meant.

It makes me so sad to think about, because I just wish that he could have lived another four years to see me play for Anderlecht. To see that I kept my promise, you know? To see that everything was going to be O.K.

I told my mum that I would make it at 16.

I was late by 11 days.

May 24, 2009.

The playoff final. Anderlecht vs. Standard Liège.

John Thys/AFP/Getty Images

That was the craziest day of my life. But we have to back up for a minute. Because at the start of the season, I was barely playing for the Anderlecht U-19s. The coach had me coming off the bench. I’m like, “How the hell am I going to sign a pro contract on my 16th birthday if I’m still on the bench for the U-19s?”

So I made a bet with our coach.

I told him, “I’ll guarantee you something. If you actually play me, I’m going to score 25 goals by December.”

He laughed. He literally laughed at me.

I said, “Let’s make a bet then.”

He said, “O.K., but if you don’t score 25 by December, you’re going to the bench.”

I said, “Fine, but if I win, you’re going to clean all the minivans that take the players home from training.”

He said, “O.K., it’s a deal.”

I said, “And one more thing. You have to make pancakes for us every day.”

He said, “O.K., fine.”

That was the dumbest bet that man ever made.

I had 25 by November. We were eating pancakes before Christmas, bro.

Let that be a lesson. You don’t play around with a boy who’s hungry!

I signed my pro contract with Anderlecht on my birthday, May 13. Went straight out and bought the new FIFA and a cable package. It was already the end of the season, so I was at home chilling. But the Belgian league was crazy that year, because Anderlecht and Standard Liege had finished tied on points. So there was a two-leg playoff to decide the title.

During the first leg, I’m at home watching on TV like a fan.

Then the day before the second leg, I get a phone call from the coach of the reserves.

“Hello?”

“Hello, Rom. What are you doing?”

“About to go play football in the park.”

“No, no, no, no, no. Pack your bags. Right now.”

“What? What did I do?”

“No, no, no. You need to get to the stadium right now. The first team wants you now.”

“Yo …. What?! Me?!”

“Yeah, you. Come now.”

I literally sprinted into my dad’s bedroom and was like, “Yo! Get your ass up right now! We gotta go, man!”

He’s like, “Huh? What? Go where?”

I’m like, “ANDERLECHT, MAN.”

I’ll never forget, I showed up to the stadium, and I like pretty much ran into the dressing room and the kitman said, “O.K., kid, what number do you want?”

And I said, “Give me number 10.”

The kitman said, “O.K., kid, what number do you want?” And I said, “Give me number 10.”

Hahahaha! I don’t know. I was too young to be scared I guess.

He was like, “Academy players have to take 30 and above.”

I said, “O.K., well, three plus six equals nine, and that’s a cool number, so give me 36.”

That night at the hotel, the senior players made me sing a song for them at dinner. I can’t even remember what I picked. My head was spinning.

The next morning, my friend literally knocked on the door of my house to see if I wanted to play football and my mum was like, “He’s out playing.”

My friend said, “Playing where?”

My friend said, “Playing where?”

She said, “The final.”

We got off the bus at the stadium, and every single player walked in wearing a cool suit. Except me. I came off the bus wearing a terrible tracksuit, and all the TV cameras were right in my face. The walk to the locker room was like 300 meters. Maybe a three-minute walk. As soon as I put my foot in the locker room, my phone starts blowing up. Everybody had seen me on TV. I had 25 messages in three minutes. My friends were going crazy.

“Bro?! WHY ARE YOU AT THE GAME?!”

“Rom, what is happening? WHY ARE YOU ON TV?”

The only person I texted back was my best friend. I said, “Bro, I don’t know if I’m gonna play. I don’t know what’s going on. But just keep watching the TV.”

p/s To read the rest of article, please click on link above

p/s To read the rest of article, please click on link above

Anthony Loke sold our Data to China

WHY DID THE MINISTER OF TRANSPORT SELL OUR DATA TO CHINA?

AT WHAT PRICE AND FOR WHAT REASON?

IS LGE INVOLVE?

WHEN POWER COMES ONTO THE LAP SO EASILY, DOES ONE NEED TO START FILLING UP OWN POCKET?

IS THIS HOW MAHATHIR CHOOSE HIS BAIT WHO ARE CORRUPTED AT FIRST SIGHT.

Perfect timing to steal

Tan Sri Muhammad Ibrahim resigned on 15th June 2018.

Datuk Nor Shamsiah Mohd Yunus became Bank Negara Governor on 22nd June 2018.

Between 16th June to 21st June 2018 US$1.91 Billion was transferred out from Bank Negara.

WHO WAS GIVEN INSTRUCTION AND BY WHOM TO DO THAT?

The plan was well planned. The scapegoat would be LGE and DAP. That is why a Finance Minister must have Economic Background and be alert at all times, especially if one is non Muslim and non Malay.

Clue number 1:

1 Mastermind who has the power from outside PH government

Clue number 2:

4 Beneficiaries

Clue number 3:

1 Bank Negara Officer who became instant millionaire. For the transfer, was given US$2 million.

Clue number 4:

THE THIEVES ARE ALL MALAY

Containing Property Prices

Many major cities are trying to contain spiraling property prices which have become unaffordable for the bulk of their own population. No need to delve too deeply into too many theories on this. The breakdown of the major factors affecting property prices as confirmed by the research paper below from BIS:

real house price growth – the perception that investors and buyers get real house price growth; i.e. returns must be higher than nominal inflation; hence the GDP growth prospects and financial balance sheet for the country must be “good-strong”

Australia’s Plate Of Worry

net migration inflows – in the 70s and 80s there were waves of migration to developed countries and that was a noted catalyst for higher prices; however from 2000 onwards we have seen the dubious flow of illicit funds from Russia and institutional flow of funds from certain countries’ pension funds in particular to the UK and other global cities; for the last 10-15 years the outflow of funds from China to certain investing hotspots have been a big factor as well; hence actual migration of people is no longer necessary as people are a lot more mobile and global in their investment portfolio

size of the existing housing stock – self-explanatory; however the more vibrant a city’s economy which will attract the better rental market, is another important supporting factor

nominal interest rates – self-explanatory

These 4 main factors may have explained much of the price growth from 70s-2000. However, there are two major factors unaccounted for, which may further explain the present stratospheric property prices:

a) the hyper-liberal ways developed nations have been printing money to get themselves out of the few financial crisis

b) the enormous wealth created in China by the middle class

“““““““““““““

Residential investment and economic activity: evidence from the past five decades

BIS Working Papers | No 726 |

06 June 2018

BIS Working Papers | No 726 |

06 June 2018

The paper studies the evolution and key drivers of residential investment in 15 advanced economies since the 1970s. It also analyses how residential investment growth affects overall economic activity and the likelihood of recessions.

Contribution

Most previous research on housing markets has focused on house prices, whereas research on housing quantities – ie residential investment – has been scarce. There has also been little cross-country analysis of the determinants of residential investment. This paper partly fills this gap. It studies the key drivers of residential investment across countries and the impact of residential investment on the broader economy. We provide novel evidence on the effects of monetary policy on the residential investment cycle, highlighting the asymmetric effects of rising and falling interest rates.

Findings

We find that the key drivers of residential investment in advanced economies are house price growth, net migration, the size of the housing stock and nominal interest rates. Importantly, rising interest rates have stronger effects on residential investment than falling ones. This could result from downward rigidity in house prices, which forces housing construction rather than prices to fall as interest rates rise. We also show that declines in residential investment are a good predictor of economic recessions.

Abstract

We analyse the evolution and main drivers of residential investment, using a panel with quarterly data for 15 advanced economies since the 1970s. Residential investment is a notably volatile component of real GDP in all countries in the sample. We find real house price growth, net migration inflows and the size of the existing housing stock to be significant drivers of residential investment across various model specifications. We also detect important asymmetries: interest rate increases affect residential investment more than interest rate cuts, and interest rate changes have larger effects on residential investment when its share in overall GDP is rising. Finally, we show that adding information on residential investment significantly improves the performance of standard recession prediction models.

“““““““““““““““““““““““

Many countries have tried to contain the price surges, from the UK, to Canada, to major cities in China, to Hongkong, to Australia and even New Zealand. Finally, I think Singapore has come up with the most brutal and (possibly most effective) policies to counter the price bubbles.

ABSD Changes (Singapore)

| AS OF JULY 5 | FROM JULY 6 | |

|---|---|---|

| Singaporeans buying first residential property | 0% | 0% |

| Singaporeans buying second residential property | 7% | 12% |

| Singaporeans buying third and subsequent residential property | 10% | 15% |

| Permanent residents buying first residential property | 5% | 5% |

| Permanent residents buying second and subsequent residential property | 10% | 15% |

| Foreigners buying any residential property | 15% | 20% |

| Entities buying any residential property | 15% | 25% (plus additional 5% for developers) |

The curtailment for local investors are quite tough but the taxes on foreigners are now quite debilitating. Other countries should try the Singapore way. It is a determined way to quash sentiment.