Four 4 days three (3) nights Poland Holiday with 3 friends should not be a culture for PH

Minister.

The amount spent was US$7,000.

Next holiday, please pay your own bills.

President Xi clever move

President Xi will be giving a very big Ang Pow to his own people.

A discount of 30% to their taxes in March.

China Chinese will have more money to spend and business will bloom.

While America and Brexit can play each other balls.

The real owner of Seafield Temple Land

The land was given free to Mokhzani Mahathir.

Mahathir’s plan B

Capital flight

In economics, occurs when assets or money rapidly flow out of a country, due to an event of economic consequence. Such events could be an increase in taxes on capital or capital holders or the government of the country defaulting on its debt that disturbs investors and causes them to lower their valuation of the assets in that country, or otherwise to lose confidence in its economic strength.

This leads to a disappearance of wealth, and is usually accompanied by a sharp drop in the exchange rate of the affected country—depreciation in a variable exchange rate regime, or a forced devaluation in a fixed exchange rate regime.

This fall is particularly damaging when the capital belongs to the people of the affected country, because not only are the citizens now burdened by the loss in the economy and devaluation of their currency, but probably also, their assets have lost much of their nominal value. This leads to dramatic decreases in the purchasing power of the country’s assets and makes it increasingly expensive to import goods and acquire any form of foreign facilities, e.g. medical facilities.

Window 9 (W9)

A window of opportunity is a short time period during which a rare and desired action can be taken. Once the window closes, the opportunity may never come again. In a competitive market with many participants seeking to maximize tangible or intangible value for their constituents, whether owners and other shareholders, employees or perhaps their community, the window will shut fast as soon as a good deal is recognized.

The Pictet Group k

Known simply as Pictet, is a Swiss multinational private bank and financial services company founded and based in Switzerland. Headquartered in Geneva, it is one of the largest Swiss banks and primarily offers services in wealth management, asset management and asset servicing to private clients and institutions.

The Pictet Group employs around 4,200 people, including 900 investment managers.[4][5] It has a network of 27 offices in financial services centres, including registered banks in Geneva, Luxembourg, Nassau, Hong Kong and Singapore.

Belgian Bank

5 Foreign Handlers

Since the rejection of Open Society to help bring stolen funds back to Malaysia, Mahathir, Daim and their children have now turn to five (5) Foreign Handlers to do the job with a promise of 30% of the funds as payment. A down payment of 10% has already been deposited to their accounts.

Between January19 2019 till March 29 2019 the five (5) Foreign Handlers will be taking out stolen funds from 2 locations in South America, 1 location in Latin America and 2 location in Europe to Pictet and a Belgian Bank.

Money will then be transfer to other foreign accounts own by ex UMNO, ex PAS, ex Amanah and ex PKR members who have sold their souls to Mahathir to make Mukhriz as the 8th Prime Minister.

Those without foreign accounts will have their goodies when these five (5) Foreign Handlers bring the balance of the stolen funds back to Malaysia.

The recent announcement by Mukhriz for the development of Kedah is just a camouflage for the funds that is coming back.

The idea to use Brexit as capital flight for window 9 is fantastic but forgetting today’s technology can reveal Mahathir’s Plan B faster than the old man can shit.

So by the end of March 2019 if the funds are well taken care of, Mahathir will be able to get his 2/3 forming the biggest MALAY PARTY without the Chinese.

Yes! DAP will be thrown out, Amanah will cease to operate like UMNO and there will be a break up in PKR leaving Kak Wan as a lame duck crying for Anwar who will be isolated under NSC for the rest of his life.

Mahathir determination NEVER TO ALLOW ANWAR BE THE NEXT PRIME MINISTER IS SEAL IN HIS HEART.

The question Malaysians should be asking and demanding to know the following:

1. Where did Mahathir and Daim get US$150 billion?

2. Who were the ones who helped legalized the stolen funds?

3. How much did Mahathir and Daim stole from 1981 – 2003?

4. Will Malaysians allow a single Malay Party to govern Malaysia without the non Malays and non Muslim participation?

5. With 2/3 majority Mahathir can change the Federal Constitution by abolishing the Sultanship especially the Agong with the Russian bride.

6. Will Malaysians be happy to have only two families rule Malaysia for centuries to come making your future generations as slaves to them?

7. Since May 10 2018 till today Malaysia economy has been diving down and down. Our ringgit has grown weaker. Foreign investors are leaving instead of coming. The increase in unemployed has risen.

8. There is an increase of 20 Tahfiz schools in peninsula and now there are plans to have 200 such schools in Sabah.

9. Why is Mahathir and Daim planning to jail Anwar under NSC, when he has not done wrong to harm Malaysia?

10. Why are there no longer fighting spirit in the hearts of Malaysians and Sultans against the plans of Mahathir and Daim?

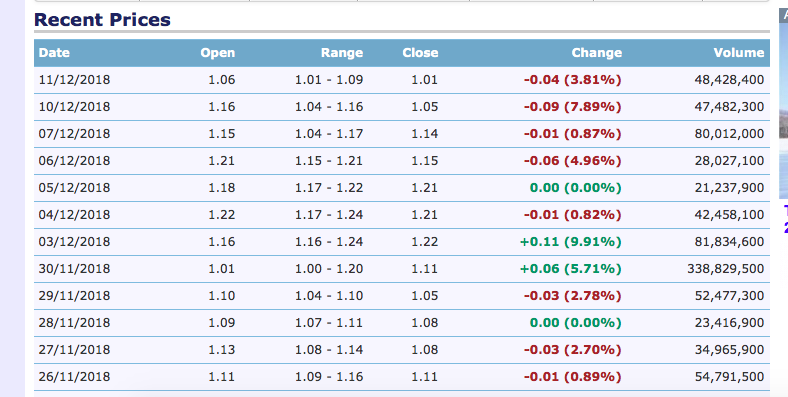

My E.G. – Unexplainable Drop?

Investors, traders and fund managers have been scratching their heads over the past week over MyEG’s share price. Just have a look:

“The company wishes to inform that to the best of its knowledge after making due enquiry with the board of directors and major shareholders of the company seeking the cause of the unusual market activity in the company’s securities, the company is not aware of any factor which may have contributed to the unusual market activity, which led to the sharp fall in share price and increase in volume recently,” it said.

Read more at https://www.thestar.com.my/business/business-news/2018/12/12/my-eg-falls-in-heavy-trade/#5V4hMkcGk4IJr6JL.99

Generally i wouldn’t bat an eyelid over stock volatility, especially in the present trying market conditions. What was galling was that the official statement from the company itself that they did not know why the stock price got hammered over the past few days.

Let’s look at the developments over the past few days:

a) There was an immense volume jump on 30 November to 338.8m shares with the majority of the shares “crossed in the market” at RM1.11 during the “price fixing slot (4.45-4.50pm)”. Crossing in the market hints of legitimacy and also can shroud the real seller and buyer if they did it via numerous accounts. As no substantial shareholder informed Bursa that they had bought/sold substantially a few days after that transaction, suffice to say, they came from various sources of buyers and sellers – but it would be clear to any market observer that tens of accounts cannot be acting in concert without “someone in control of the situation”.

338.8m shares a day is almost 10% of its number of shares outstanding. That amount of shares being traded, with the bulk at 4.50pm all in one go. Hard t fathom that it was all minority shareholders deciding to sell and buy all at once.

b) The stock traded up 11 sen on 81.8m shares the next day but subsequently has been falling like a rock continuously till the big drop today: down 17 sen to close at the day’s low of 84 sen on 231.8m shares traded.

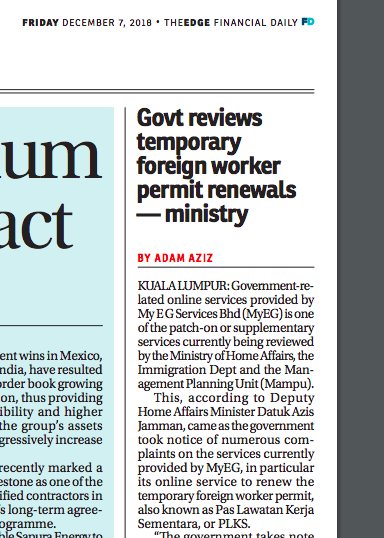

c) The government announced on 7 December that it is reviewing temporary foreign worker permit renewals, which affected MyEG’s business outlook for sure if they were to lose the business.

Hence one of the first question will be: “did the sellers knew of this news on 30 November?”

It would be too simplistic to think the sellers knew something that they buyer doesn’t. In many collusion cases, both sellers and buyers KNOW about the impending market moving news. Sometimes the “sellers” are more important, and need to sell first without people knowing. The buyers then sell again in the market later. I am just guessing here. Or it may be NOBODY knows anything and it was a straight forward market transaction. Anyhow, Bursa and SC should investigate so as to provide all investors with a clear picture that nothing untoward actually happened. It is important for market integrity.

d) Even more interesting was that on 27 November, the company announced potential e-govt projects in Indonesia. This can be surmised as positive news as it might be able to transplant similar business model and business knowledge in a less “politically motivated” environment.

e) If the 7 December news was “so bad”, the selldown would have happened immediately, but no, it did not.

f) So was it a margin shortfall situation like Seacera. Possible but we don’t know. Judging by the flow of events, a margin sell down by a substantial shareholder could be probable, and if that’s the case the company should not say they don’t know what happened.

g) The company and TS Wong have been busy buying shares for the past few weeks. I am going to leave the facts there. EPF announced on 12 December that it is now a new substantial shareholder with in that they have acquired 29.5m shares. Doesn’t look too good for EPF to have bought and see the stock crater the next day.

Conclusion: I am not saying there were any shenanigans over the last 2 weeks but for the company to say they were unaware is a bit hard to stomach.

Mahathir fighting Dementia and Time

Our Mission

The Open Society Foundations work to build vibrant and tolerant societies whose governments are accountable and open to the participation of all people.

We seek to strengthen the rule of law; respect for human rights, minorities, and a diversity of opinions; democratically elected governments; and a civil society that helps keep government power in check.

We help to shape public policies that assure greater fairness in political, legal, and economic systems and safeguard fundamental rights.

We implement initiatives to advance justice, education, public health, and independent media.

We build alliances across borders and continents on issues such as corruption and freedom of information.

Working in every part of the world, the Open Society Foundations place a high priority on protecting and improving the lives of people in marginalized communities.

Our Values

We believe in fundamental human rights, dignity, and the rule of law.

We believe in a society where all people are free to participate fully in civic, economic, and cultural life.

We believe in addressing inequalities that cut across multiple lines, including race, class, gender, sexual orientation, and citizenship.

We believe in holding those in power accountable for their actions and in increasing the power of historically excluded groups.

We believe in helping people and communities press for change on their own behalf.

We believe in responding quickly and flexibly to the most critical threats to open society.

We believe in taking on controversial issues and supporting bold, innovative solutions that address root causes and advance systemic change.

We believe in encouraging critical debate and respecting diverse opinions.

************************************************************************************

I simply love what is happening to my country. First we have the classless arrogant Malays running amok in protest of something they do not understand neither do they wish to learn more what ICERD really means.

Malays are always condemning and bad mouthing the Jews, yet they love everything that are produced by the latter.

In Quran it clearly state THAT NO ONE IS BORN INTO A RELIGION BUT TO A PARTICULAR FAMILY. But the Malays here claim they are Muslim by birth. What the fuck. Did their children go through a religious rite to be Muslim? In fact these so called Muslim are Kafir themselves.

In Quran it states one need to pray at least twice a day. So where did the five times prayer come in?

In Malaysia it is not a crime for the ruling Government to steal, murder, blackmail, commit adultery, incest and lie at every opportunity but not for the ordinary citizen of its country.

In Malaysia a title open the doors to crime but not honesty and dignity.

Malaysia held its GE14 on May 9th 2018. The battle against the most corrupted Government came to a sweet end but ……………………………

Mahathir became the 7th Prime Minister but what happens????????????

Malaysia went back in time to 1982

This time round those loyal guards around Mahathir either have gone to the next world or are lost through the passage of time to understand how forward the world has moved on.

So where does New Malaysia stand?

With the Malays determination to destroy the Economy and its dignity, there is no hope. Everything wrong in Malaysia, the blame goes to DAP, the Christians, the Chinese, the Indians and the Jews but never themselves.

Malays today have lost the value of living and are behaving like zombies.

So given every opportunity a new drama unfold.

The latest drama is Mukhriz the son of Mahathir who also happens to be the Menteri Besar of Kedah for now.

He wants to bring back RM150 Billion hidden in four (4) countries back to Malaysia to buy the 8th Premiership. Mukhriz’s people have been going to Europe to seek help.

Several businessmen are forking out RM30 Billion to form an NGO. This NGO will later be a new political party for the coming GE15. The funds are also hidden overseas in seven (7) countries and they too seek foreign help to bring the money to Malaysia.

Najib and Rosmah’s people are seeking help to bring back RM2 billion for reason unknown.

Now who says Malaysia has no money. There is plenty to upgrade and modify Malaysia into a new world but these rich people are selfish. Everyone think they can be the 8th Prime Minister.

So Anwar is not the only one going for the Premiership after Mahathir.

I would like everyone to note this.

Mukhriz and his people are seeking the Open Society to bring back RM150 Billion for him to be the 8th Prime Minister.

Businessmen are forming an NGO to bring back RM30 Billion through Open Society to be a political party for GE15.

Najib and Rosmah’s people are seeking the Open Society to bring back RM2 billion.

I AM NOW WAITING FOR THE MALAYS TO FOAM IN THEIR MOUTH AND HOLD ANOTHER PROTEST AGAINST THE JEWS, SOROS AND THE OPEN SOCIETY WHILE MAHATHIR IS SHOWING SIGN OF DEMENTIA.

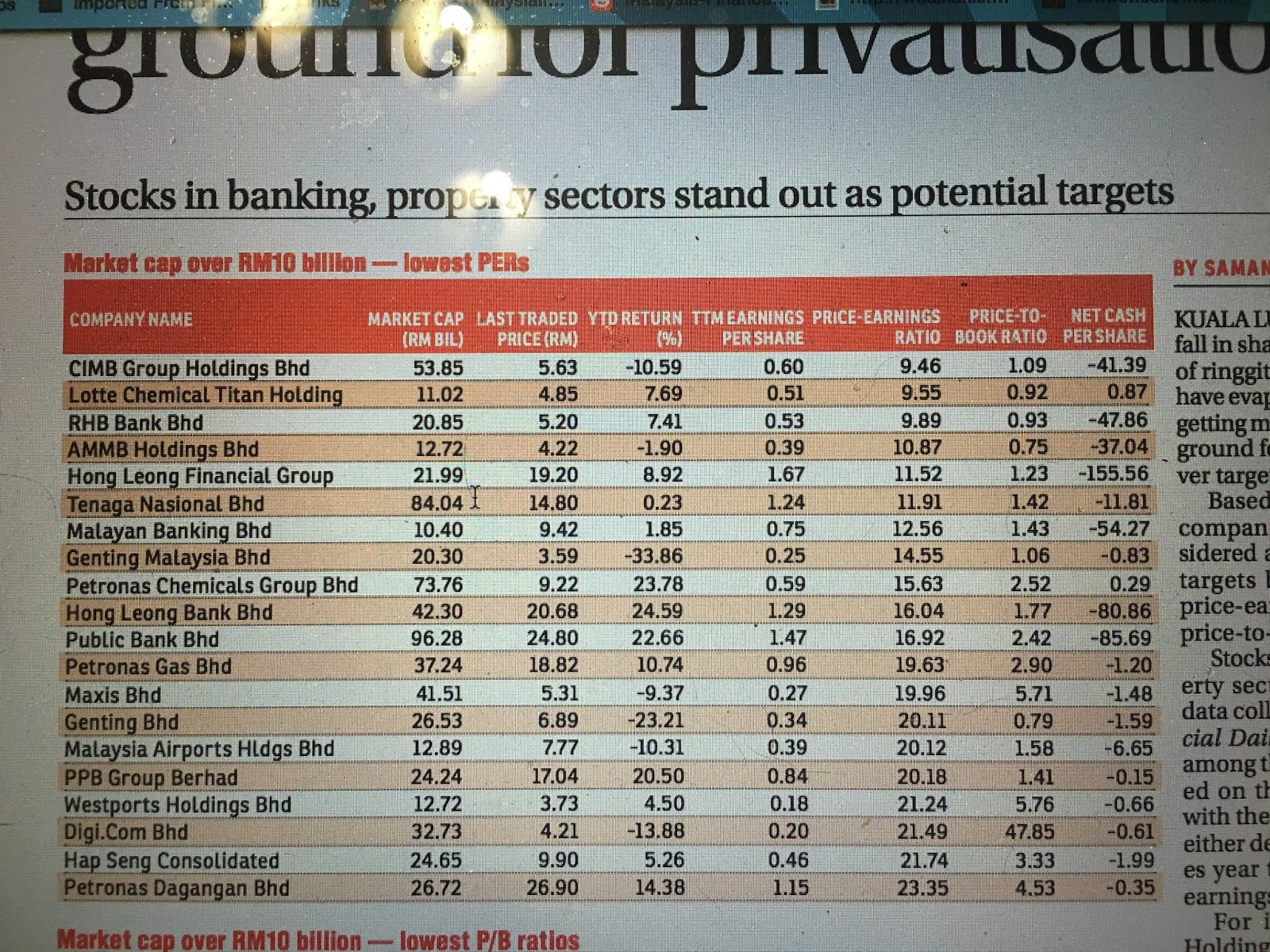

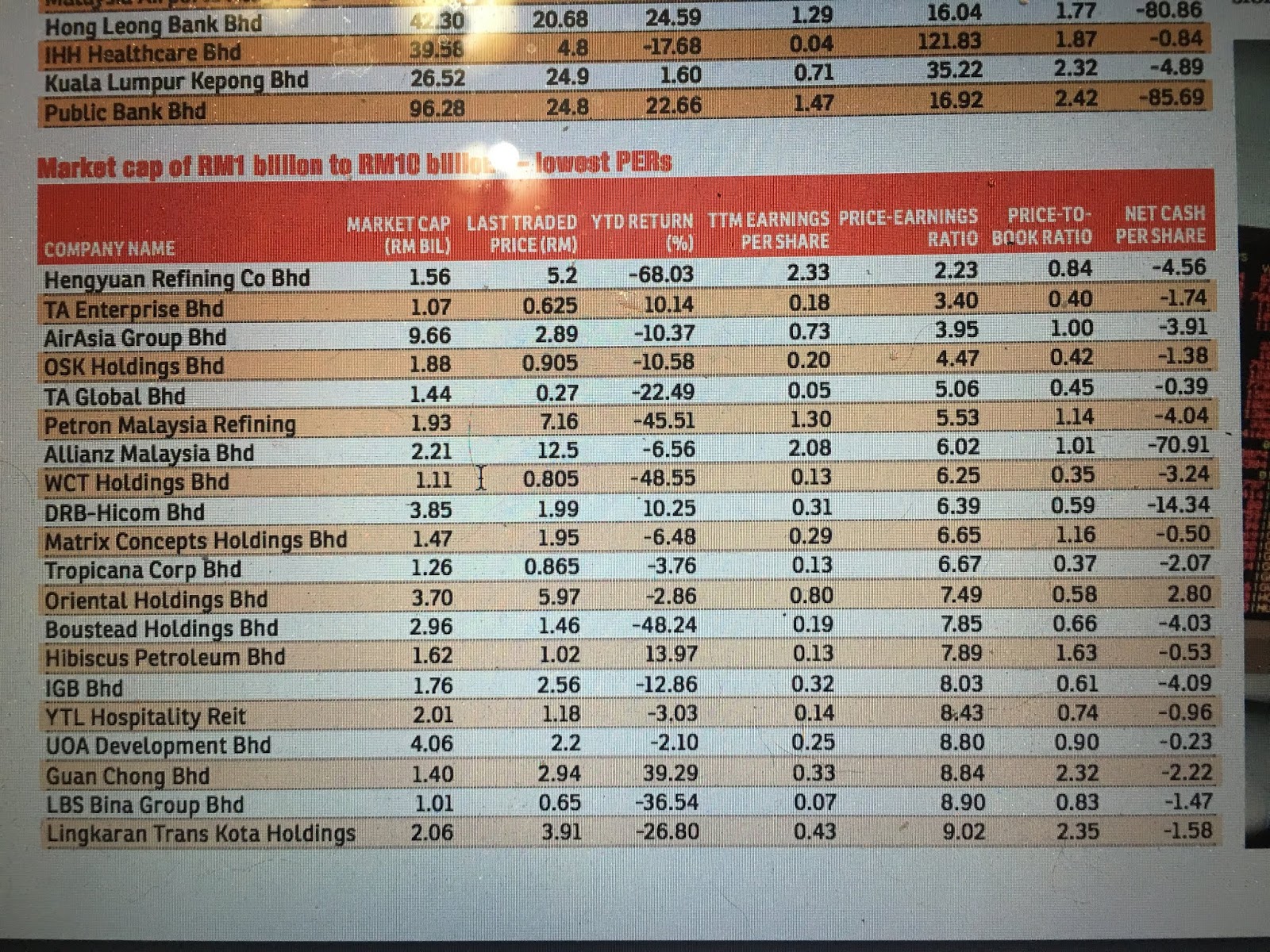

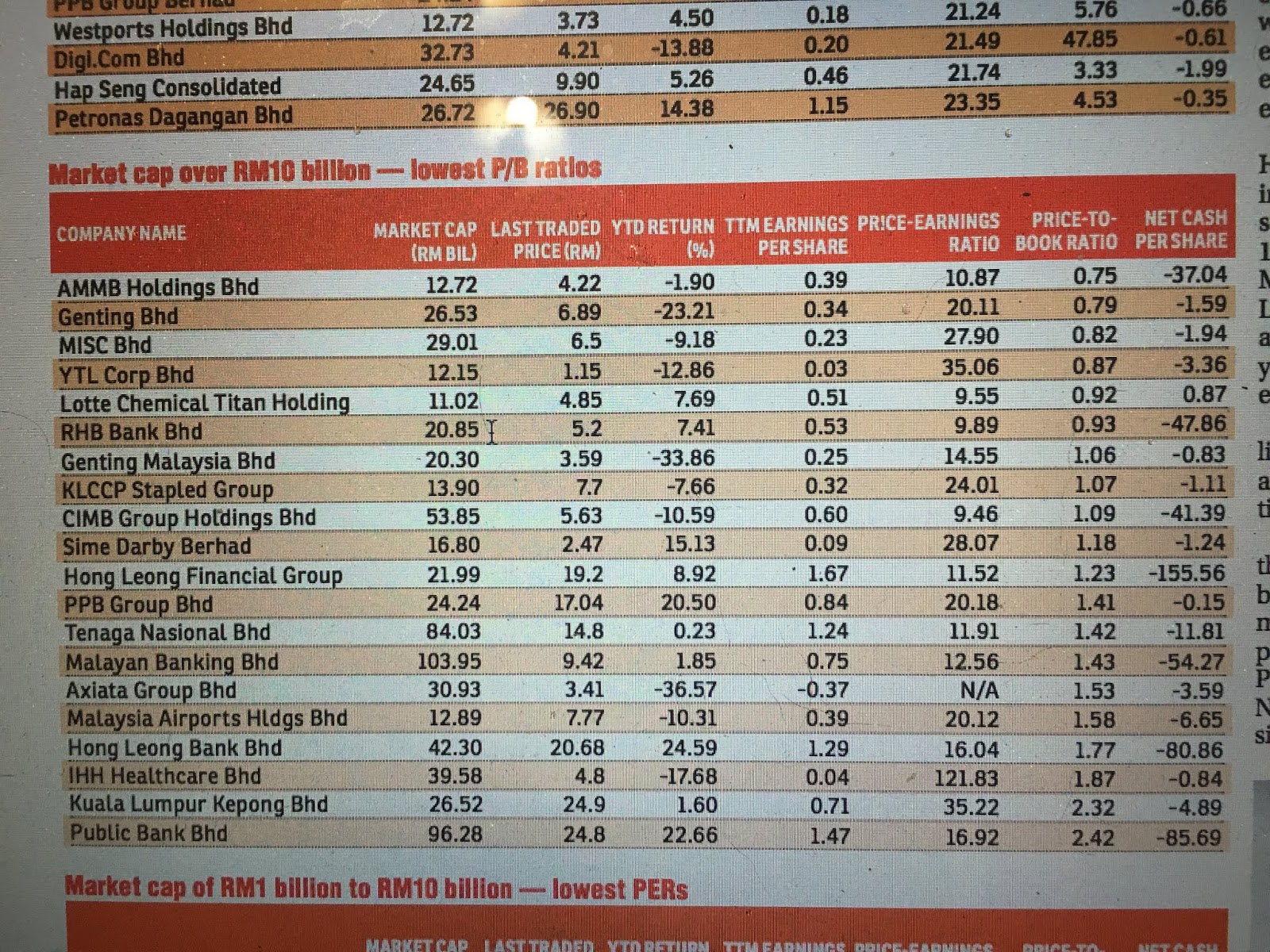

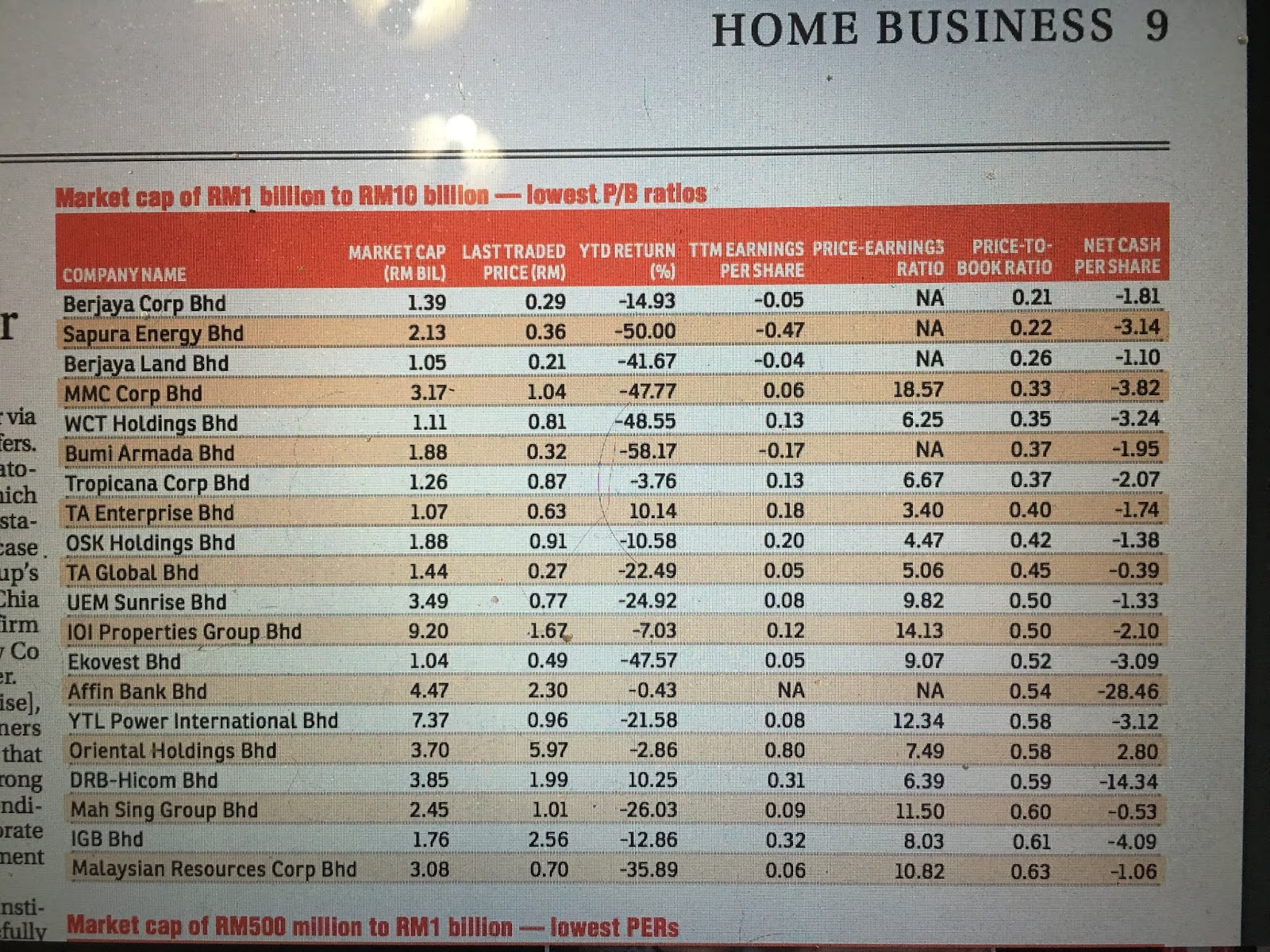

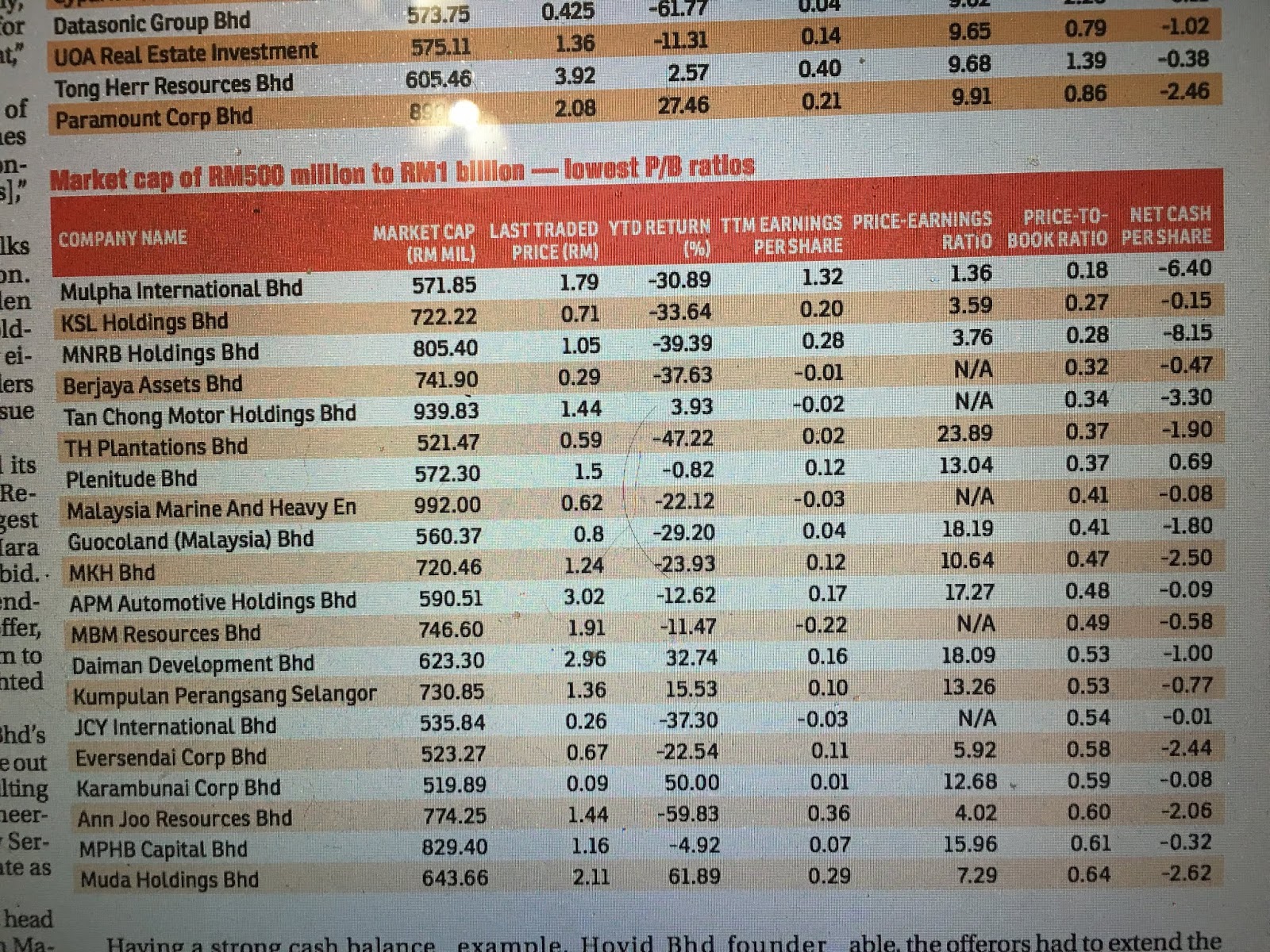

Low PER & Low P/B Ratio – Privatisation/Investing Candidates

The Edge did a marvellous compilation on stocks with low PER and low P/B, citing considerations that there may be plenty of opportunities for privatisation. Let’s look at the low PER first.

Granted the equity markets have been in the doldrums for sometime now, hence as a collective group PER valuations would move down. It has to do with what we call “earnings visibility”.

Privatisation is seemingly easy to suggests but the reality for most listed companies, even when their PER or PB are low, they needed the access to capital markets via their listing vehicle. Hence to take them private be it the owners themselves or PE funds, they probably have to tag another extra 30% as capital needs as each privatisation will need to wait it out maybe 3-5 years before relisting.

PER SECTION

a) PER refers to the earnings ratio. Hence there are a few assumptions, PER is only a valid reading if its a “going concern”. PER has to do with earnings predictability. How low is deemed as low? Well it varies according to the industry they are in.

Product life – Easy to explain if its steel products or oil palm earnings, the paradigm rarely shifts much. Even when its cyclical one can argue that it is predictable as the four seasons. However, some products, esp technology based, require reinvention and R&D spending cause products can be obsolete within a shorter cycle (3-5 years). Which is why every new I Phone will hit share price of Apple up or down every 2-4 years.

Predictable Margins – This should be the most important factor for high/low PER. If you are capital intensive (steel) your margins are going to be low, which partly explains a lower PER range. Same for tech companies which should command higher margins and as such higher range of PER.

Thus we cannot say just shoot for the 5 lowest PER stocks for investing purposes or prvatisation.

b) The Banks – The banks are quite attractively priced in terms of PER now compared to historical range. Earnings is clouded becaus enothing much is moving. Equity markets very slow, investment banking very slow, property loans even slower. But thats the present and the immediate future (1-2 years out). If you are considering as a long term investment, banks look good, if you want a proxy on a recovery in 2-3 years, banks would be excellent. Its not like any of the top few are losing money.

Should you privatise then? It takes a hefty sum to privatise plus tack in another 2% in fees. Then most probably you need to relist, which might take 3-4 years out in this scenario to get a better valuation. Plus the valuation then must be lucrative enough (e.g. maybe in the 30-40% range). Can we relist CIMB in 3 years at 15x, maybe.

But the biggest obstacle in the period when it is privatised, as banks are capital hungry vehicles. Can the funder also fund the capital requirements. Which is why banks are usually out of the question when it comes to privatisation opportunities.

c) Genting Malaysia – Hit very hard by higher duties and taxes in the recent Budget, and got hit again by the Disney/Fox legal issue. Investors must be very careful to use historical prices and PER for Genting Malaysia to base their investing decisions. The whole earnings structure, in particular margins, have shifted substantively. The previous high will be insurmountable in today’s rules.

GM will earn a lot less for every ringgit. The upside is that now GM is highly uncompetitive in the region – in that the government would have very little room to further raise taxes and duties on GM in the future. Now that it second in the region in terms of duties and taxes.

So, another no-go candidate for privatisaton. Share price will have to hit RM2.50 before the Lim family should do any serious privatisation considerations.

The rest in the first table still have exceedingly high PER valuations, e.g. Maxis, Westport, DIGI.

d) Hengyuan Refinery – Two to three x PER, where to find??? When something is so cheap, there must be a catch. The catch would be that the previous earnings which the PER is based on is not sustainable, or in fact is likely to dip substantially in the future. You need to do a lot of research first for this stock, not as plain as it looks.

e) Air Asia Group – This 4x PER is pretty ridiculous. It is very much a going concern, and even if it stops operations, P/B is at 1.0x which means you should be able to sell most assets and get back your money. I give you RM5bn and you try and build another AirAsia. This could be a good stock to look at for short or long term.

The auto makers, brokers, insurance and property counters are about there, and nothing terribly exciting, no one will be thinking of privatisation.

f) Stocks like Mulpha or TA Global, nobody really knows what they want to do or are doing. They might not do much over the next 10 years. No point looking at them. You get charkuayteow at 20 sen a plate also no use as the horfun is made of plastic.

g) Politically Out Of Favour – Without needing to name names, they should be forgotten in the new era, earnings visibility ZERO.

h) Paramount Corp – At 10x, looking very interesting but I think it needs to get to 7x before they will act.

P/B SECTION

P/B is a low confort investment factor. P/B is only relevant IF the company is bundled up and sold in pieces or as a whole. Too many vehicles have too many local funds and government interest involved that they won’t be sold even if Blackrock makes an attractive offer.

a) KLCCP Stapled – PB at 1.07x. This one is interesting because we are talking about the creme de la creme of property REIT. Highly desirable if it drop to 0.95x.

b) Owner Driven – Many of these owner driven counters have shocking low PB. Well, if the owner also don’t want to privatise at 0.3x, why would you want them? The exception maybe is Tropicana Corp, which has astutely offloaded a lot of Johor land last couple of years. Tropicana with a PB 0.37 has reached a level that makes it highly attractive to privatise.

Some of the property companies has a low Pb ratio too but you have to assess how “realisable the bulk of the assets (land bank) are”.

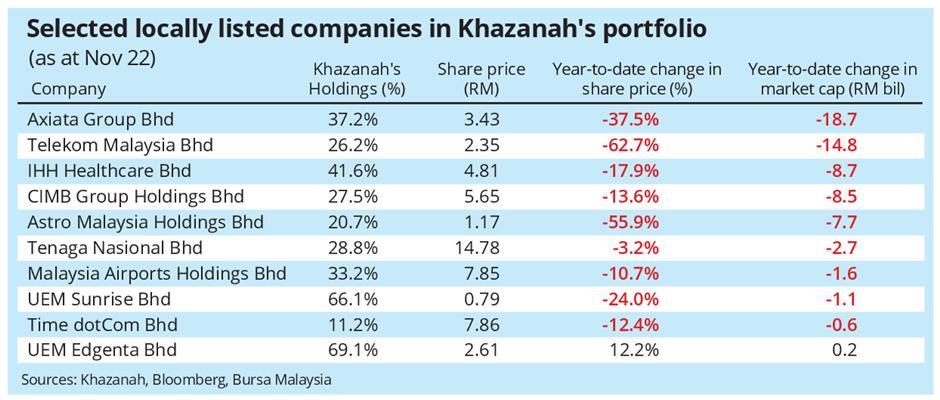

Khazanah’s Portfolio Assessed

Khazanah’s portfolio makes for a very interesting read, but probably not for the reasons you are thinking. Yes, the markets have been bad. It would have been a very cheap shot to snap a portfolio’s performance at ONE specific date and try to “shame” the managers. That is not my intent and I don’t think Star Biz wanted to do that at all.

a) Performance – It is in line with the rout in global equity markets, more so for emerging or developing markets. The trade war exacerbated the situation.

b) Key Holdings – Mind you, these are key holdings, or substantive holdings of the said company, hence it is not like you can trade in and out easily.

c) Blame – Well, even in a rout you have losers and real outsized losers. Could Khazanah have known or impacted on those companies. We are talking about Axiata, Telekom and Astro in particular? They could only make their input at board level. Failing which, they could have initiated a replacement of the CEO with someone with a better strategy and execution ability to navigate the changing landscape or difficulties within operations. On that level, yes, some blame could be attributed to Khazanah.

d) In Line – The rest, the losses were understandable and in line. Even UEM Sunrise would have a down trodden property market to help explain its performance.

e) Crowding Out Effect – Curiously, the best lesson to be learned from the table is the crowding out effect, or lack of rather. I used to hammer home the point that the big danger for Malaysian equity market is that local funds are getting much too much funds flow, and together they keep holding an increasingly larger and larger slice of the ownership of key index component stocks.

The follow on thesis is that at a very substantive level, the local funds may be able to “control” prices of selected stocks which would then give an unfair picture of the true worth of their holdings. If retailers and foreigners keep selling, and local funds keep buying, technically prices wouldn’t change. But the table above showed clearly that NONE of that is happening – which is a good thing.

Conclusions: Khazanah, and other local funds which hold substantial stakes in listed firms, must be more proactive and vigilant in assessing the direction, strategy and operations of the said companies. Questions need to be asked more frequently whether they are aware and prepared for the forever changing competitive landscape and shifting economic paradigm they are operating in.

In my view, too often the CEOs of GLC linked firms are given too wide a berth to manage the companies. Are they mere messengers to comply or are they active agents for change and improvements? The hiring and firing must be swifter. You dilly-dally you get FGV.

On that note, EPF has a brewing problem at RHB Bank. The rapid departure of many key staff did not happen just the last few months. You can trace it back as far as two years but NOTHING changed. As a cursory member of the financial industry, one can see that there are huge problems at RHB. Anecdotal hearsay: too many decisions done by committees, HR is the most powerful department there (not in a good way), the old guard act like gatekeepers and not many are keen to stick their necks out for taking on more risks. Only now we are talking about changing CEO. In my view, not just the CEO but probably another 10 top people there needed to go as well.

Cabinet Reshuffle in December 2018

Mahathir is holding the cards close to his chest for the coming reshuffle.

WILL THERE BE SURPRISES OR SHOCK WAVE THAT CAN ROCK THE NATION?

But like most Malaysians after PKR election, we know Mahathir will as usual change his Deputy to someone who promised to make Mukriz the future Prime Minister.

The fact that Anwar already said he does not want the Deputy Prime Minister post but the Prime Minister seat make it easier for Mahathir to replace Kak Wan with Azmin Ali.

Mahathir today and the past are the same except in age when it comes to the issue of Anwar.

Now that the main cast is put in place, who then will be move?

Two have been given a year to live so they have to go.

One being kicked out from the State.

Two make a mockery of their position as Ministers.

One who can only work if given a title.

One who demand for 30% commission on every task given by her Ministry.

One who could not sell our bonds and bring in investment.

SO WHO ARE THE LUCKY ONES IN THIS GAME OF CHESS?

SELANGOR JERKOPOTAMUS

In Malaysia it is hard to find a caring leader who can lead with honest heart and open mind.

Every single Melayu that sits on high post tends to forget they were chosen to serve the Rakyat.

Selangor is a rich state with plenty of resources and close to ports which make it a strategy place to do business.

Lots of land and assets have been siphoned off in recent times.

Both by UMNO and PKR leaders.

Even though Selangorians choose to close their eyes on the theft in the past, many are now talking about it because the stealing is now closer to their home.

Politicians who declared their wealth with MACC are falsely putting figure that does not jive with the kind of money they have in Swiss Bank, Hong Kong, Singapore and Australia.

How much can a full time Politician earn in a month or a year?

If one were to calculate their salary per month together with their spouse and maybe 4 to 6 children from just 1 wife. Can the take home pay be RM8 million?

MACC and PDRM should be serious in their investigation over the actual income each politician receive per month.

PKR took over Selangor in 2008. Khalid a millionaire was chosen as the 14th Menteri Besar of Selangor and was forced to give up the seat in 2014. During that period his wealth rose up RM2 million.

Then Azmin became the 15th Menteri Besar. Azmin and family was worth only RM5.2 million then. Today Azmin, wives and children have assets worth RM2 billion and have several Swiss Accounts which BIS is happy to give the hard copy.

Zuraida before Azmin was MB had assets of only RM300,000. Today she is worth over RM300 million and her toy boy has over RM20 million. She too has Swiss accounts.

Amirudin had just join the Swiss Club and is worth more than RM60 million. In 6 months money went after him instead of the other way round.

Now that Amirudin is rich beyond his dream he forgets that Selangorians work in their sweat to earn a living.

Most Selangorians fall in the M40 and B40 category.

The coming 6 months many will be without a job or have their salary cut because no foreigners want to do business in Malaysia, neither do they want to lend money to us because Politicians like Azmin, Zuraida and Amirudin are also dirty crooks like Barisan Nasional people.

Many foreigners are shaking their heads that Malaysians can blindly donate over RM200 million to the Harapan Fund while their leaders continue to rob this nation.

Not enough, now Amirudin wants to cut off the free 20 meter of water to all Selangorians and only give it to the B40.

I find it hard to digest that now Selangorians have to pay more for their water so that B40 can have free water, while people like Azmin Ali and Amirudin siphoned off the commission from Splash to live in luxury.

The other unacceptable fact is Amirudin has again divided the people into classes.

First we have the race, then religion and now different class of people – the filthy rich, the rich, the middle and lower class. What about the 30% Bumiputra right? Does the Chinese, Indians and others have that privilege too?

In the end we are being fuck and screw at every direction just to make an MB popular.

I TRULY BELIEVE IF AZMIN ALI, ZURAIDA AND AMIRUDIN CAN RETURN THE DONATION, COMMISSION AND GIVE US BACK ALL THE STOLEN LAND WHICH IS AROUND 200,000 ACRES, SELANGORIANS CAN RECEIVE NOT 20 OR 25 METER BUT 50 METER OF FREE WATER FOR THE NEXT 12 YEARS.