How should one play the “coronavirus” as an investor? Should we even invest at all? Isn’t there something “not quite right” about making money out of certain people’s sufferings? If you bought certain stocks which jumped owing to the coronavirus, is it evil to think in your heart that the longer the virus spreads, the better my returns?

So what is ethical investing anyway? Do these funds shy away from these healthcare-related counters? Do you buy and hold fire extinguisher companies that benefited enormously from the unrelenting Aussie bushfire??? Where do you draw the line? Do you even bother in the first place?

Hence, my views here are not an indication of my values barometer. I assess these stocks as an investment option. How the situation develops is part of the fundamentals’ story. So, please, leave your principles, values, morality and political correctness behind.

Momentum Investing

You can try to rationalize why you shouldn’t jump in, but you cannot block a momentum rally owing to a significant perk in “substantive factors” in a stock’s earnings prospects.

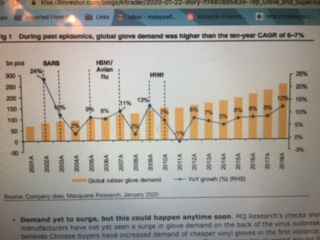

Demand yet to surge, but this could happen anytime soon. MQ Research’s checks show glove manufacturers have not yet seen a surge in glove demand on the back of the virus outbreak. MQ Research believes Chinese buyers have increased demand for cheaper vinyl gloves in the first instance. If the outbreak is prolonged, there could be a spillover to rubber gloves. The upcoming travel period around the Lunar New Year holiday could spark an acceleration of the outbreak and spur global glove demand.

Who will be the biggest beneficiary? Glove manufacturers are running close to an optimal utilization rate of 85%. Thus, any spike in demand could tilt the pricing power back to the manufacturers. MQ Research believes manufacturers with the highest exposure to the Asia market and with the highest capacity additions could be the biggest beneficiaries in terms of sales volume from this virus outbreak. Among glove manufacturers, Top Glove has the highest capacity additions, while Supermax and Sri Trang have strong exposure to the Asia market.

Biggest Consideration: Utilisation Capacity, Product Mix & Clientele’s Region Exposure

MQ Research believes manufacturers with the highest exposure to the Asia market and with the highest capacity additions could be the biggest beneficiaries in terms of sales volume from this virus outbreak. Among glove manufacturers, Top Glove has the highest capacity additions, while Supermax and Sri Trang have strong exposure to the Asia market.

Of MQ Research’s covered stocks, MQ Research prefers Top Glove over Hartalega due to its wider product mix, diversified market exposure as well as the potential benefit it could see from this virus outbreak. Nonetheless, Hartalega could also benefit if customers in developed countries (Europe and United States) start stocking up on rubber gloves as a preventive measure.

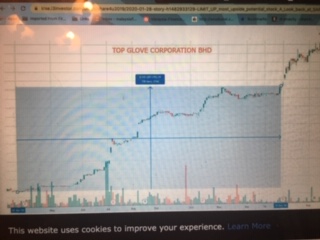

Is It Too Late To Get Into The Big 4?

The Big 4 Heavenly Stars: Top Glove, Hartalega, Supermax, and Kossan. Yes, it is late if you get in NOW and you are a trader (i.e. window period of less than a week). No, if you planned to hold. Just look at the long long term charts (2003-now) of some of the Big 4.

You cannot fully anticipate the outbreak of each epidemic, but rest assured epidemics or health scares will be the norm moving forward owing to the mutation abilities of viruses. As long as you buy and keep, EVERYBODY makes money from glove makers. You are even more “secured now” as the Big 4 have reinvested heavily and now carries a huge moat around their business that will be hard to knock off from their perch.

Even the “political collateral damaged” Supermax maintained its long term outperformance since 2003 till now.

Just look at the lovely rise over the years for these stocks. These are stocks you can keep and keep and reinvest.

What About the Newer Players?

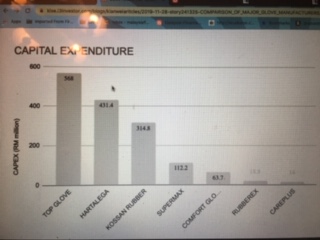

You mean Careplus and Comfort. well, just look at these two tables:

Capital expenditure can do a lot of things for the same companies in the same industry. But when the bigger players have the bulge bracket, it is very hard to even be competitive in terms of margin. Even if demand jumped 3x, they do not have the capital to take advantage of the situation.

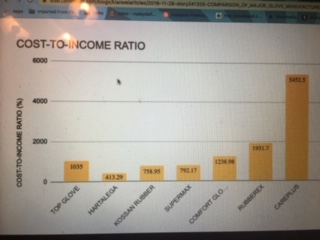

Cost To Income ration, again in almost any other industry, there will be niches you can explore. However, the overwhelming size of the Big 4 will make it inevitable that every single resource will cost the small guys more. The Big 4 have economies of scale in almost everything.

OCNCASH, Only Small Player I Like

Oceancash Pacific Berhad, together with its subsidiaries, is engaged in the manufacture and trading of non-woven products and thermobond felts for thermal and acoustic applications in Malaysia. Its products are used in various applications, including the interior and exterior trims of automobiles, and noise damper for the compressors and outdoor units of split unit air-conditioners, as well as insulation in buildings including roofs, ceilings, walls, partitions, and floors as carpet underlay. The company is also engaged in the manufacture and distribution of thermobond and airthrough nonwoven cloth and polyethylene film for hygiene applications, which include top and back sheet of diapers and sanitary napkins, and wet wipes, as well as surgical apparel, such as caps, masks, and gowns. In addition, it produces laminates of nonwoven and PE films for various applications. Oceancash Pacific Berhad is headquartered in Bandar Baru Bangi, Malaysia.

Oceacash is involved in wide ranges of hygiene manufacturing of diapers, sanitary napkins, wet wipes, surgical apparel, caps, masks and gowns.

Today was only the first day it jumped. Even so, its market cap is still just RM180m on just 245m shares. The hygiene business should dominate proceedings. I think RM1.00 is around fair for a company that happens to be in the right sector, plus with a fantastic correlation to supplying Malaysia’s best selling car.

We remain positive on Oceancash’s (OCP) business outlook after our recent meeting with management. We continue to like OCP, considering the i) favourable growth prospects in the hygiene’s nonwoven segment, ii) steady contribution of foreign felt sales from Thailand and Indonesia, as well as iii) strong management team with in-depth technical know-how. At 10x 2020E PER on the back of a projected EPS growth of 33% for 2020E, OCP’s valuation looks appealing. We reiterate our BUY call with an unchanged price target of RM0.61. This note marks a transfer of coverage.

Foreign Felt Sales to Drive Insulation Segment Growth

Profitability of the insulation segment was flat in 9M19 despite higher felt sales (+6% yoy) as this was largely offset by weaker PBT margins (-1ppt to 18.7%, exacerbated by adverse forex movement in 1H19). Prospects wise, we believe the increasing contribution from Thailand and Indonesia (foreign felt sales accounted for c. 61% of 9M19 insulation revenue) should be more than sufficient to cover for the expected shortfall in local felt sales (est. 2020 TIV forecasts lower by 1% to 590k units).

Insulation Felt Plant in Thailand Should be Ready for Action by 2H20

Elsewhere, construction of the felt production facility in Thailand remains on track to be completed by 2H20, and OCP is planning to relocate one of its two existing Malaysian production lines to tap into 1) the strong demand for resinated felt and 2) increase utilisation of excess capacity (current utilisation rates: est.50%). Locally, we understand OCP has been supplying felt to Proton refreshed models (ie. Saga, Iriz and Persona), and with this track record, the company is hopeful to participate in the Proton Complete Knocked-Down (CKD) X50 supply chain moving forward. We think OCP may give the CKD X70 contract a miss due to unfavourable pricing, similar to our observation of other auto-parts players.

Hygiene Segment’s Margins to Benefit From Cheaper Resin Cost, …

Outlook for the hygiene segment still looks promising – 9M19 PBT rose by 10% yoy to RM2.5m, on higher revenue (+1% yoy) and improvement in PBT margins (+0.5ppt to 6.1%). We believe the cheaper resin cost (est. 80% of hygiene’s raw material costs) will likely see an uptick in hygiene’s margins in the coming quarters.

Source: Affin Hwang Research – 3 Jan 2020

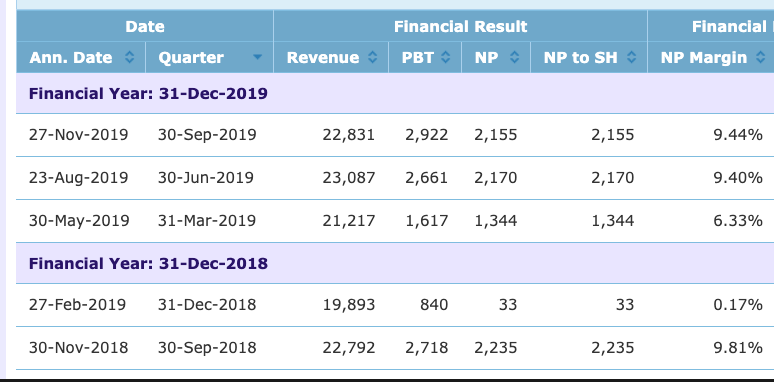

Well managed, look at the steady earnings. Now what if PBT jumps by 100% over the next 2 years. Is RM180m market cap still valid???

{kind=link}