Category: Uncategorized

Will Malaysians allow Human Gods to decide on 9th May 2018?

WILL MALAYSIANS ALLOW THEMSELVES TO BE CHEATED ON 9TH MAY 2018.

ONLY 2 (TWO) SULTANS REMAINED NEUTRAL WHILE THE REST, ONLY ALLAH KNOWS WHAT THEY ARE THINKING AND HOPING FOR.

IT IS WITH THIS KIND OF SICKNESS MALAYSIANS ARE HOPING TO CHANGE THE PRESENT CORRUPTED GOVERNMENT.

GOD EC WILL PLAY HIS ROLE BECAUSE HIS CLOSET REMAIN TIGHTLY LOCKED UNDER THE WATCHFUL EYES OF SPECIAL FORCE.

I KNOW, YOU KNOW AND THE WHOLE WORLD KNOWS NAJIB AND BARISAN NASIONAL HAVE ALREADY LOST.

R.A.H.M.A.N HAS COMPLETED ITS TASK.

THE NEW ERA OF M.A.H.A.T.H.I.R HAS BEGUN AND NOBODY PHYSICAL AND SPIRITUAL CAN CHANGE THAT.

THE LAST OF THE RUBBER TAPPERS?

In 2008, Pak Man (not his real name), a rubber tapper from Kedah was earning MYR4000 a month—a comfortable living. Today, he earns five times less—MYR800 a month.

The sole breadwinner for a family of nine children, Pak Man is struggling to eke out a living on his 3-acre lot of rubber. On a good day, he can get up to 40 kilos of latex; nowadays in the dry season of January to April, he averages about 15 kilos.

In 2008, a kilo of latex was sold for about MYR7, depending on world rubber prices. Today, Pak Man is selling at MYR1.80 per kilo, almost four times less. Responding to global markets, the price of rubber is volatile—causing large fluctuations in Pak Man’s income.

At the same time, Pak Man says that costs have gone up by more than 50%, in part due to GST. Maintaining rubber trees is no easy task—each of the 700 trees on the lot must have pesticide applied, fertilized, and treated if there are termites. Below is a comparison of prices from 2013 to 2018:

Pesticides (2 barrels per application, 3 times a year): 2013—MYR35 per barrel/ 2018—MYR55 per barrel

Fertilizer (12 bags per application, 3 times a year): 2013—MYR70 per bag/ 2018—MYR105 per bag

Pesticides (2 barrels per application, 3 times a year): 2013—MYR35 per barrel/ 2018—MYR55 per barrel

Fertilizer (12 bags per application, 3 times a year): 2013—MYR70 per bag/ 2018—MYR105 per bag

As he explains the rising costs one by one, Pak Man sounds increasingly resigned.

“My costs have gone up while my income has gone down. I have to work on others’ rubber estates to earn money on the side.”

For those who don’t know, rubber tapping is very labour intensive, requiring Pak Man to start tapping at 7am till 12pm. Paddy farming is quite different. There are generally two harvests a year—in between which farmers are able to take on other odd jobs.

Even government subsidies have dwindled. 5 years ago, the authorities would provide 24 bags of free fertilizer per year; now, only 19 bags are parcelled out.

Furthermore, those who register late are disqualified from receiving aid.

“Life as a rubber tapper is one of uncertainty. Rubber prices can be very volatile—some months we can live comfortably, other times our entire family of 10 has to share one ‘ikan kembung’ (mackerel) for dinner.”

While this year, it was announced that rubber tappers would be given a one-off incentive of MYR600, for Pak Man, it’s too little too late.

“What can I do with that money? It’s not a sustainable solution.”

“The government should step in and do something for us rubber tappers. This issue has been brought to Parliament so many times already—and still, no action.”

“Uneducated people like myself…that’s why we pay taxes so government officers can help us. What have they done for us?”

Despite his self-effacing talk, Pak Man is extremely well-informed. He’s aware of the movement of global commodity prices, government manifestos for the industry, and of the potential of downstream rubber products.

“We could be so much more. I remember reading former Prime Minister Abdullah Badawi’s plan for Malaysia’s rubber industry. More factories, diversification of products, transforming our tappers to more than just raw material providers.”

Pak Man may be the last generation of rubber tappers in Malaysia. At 60-years-old, he is wondering what will happen to his land, passed down from his father and before him his grandfather.

“One day, there will be all these tall and straight rubber trees planted in orderly lines, and not a soul around them.”

“That would be like a ghost story, wouldn’t it?

”

By Karim Raslan

Malaysian Government Cheating New Election

Eulogy for Najib and Rosmah

Eulogy as define in google dictionary is speech or piece of writing that praises someone or something highly, especially a tribute to someone who has just died.

Finding suitable words to praise a criminal is not easy especially when they are Najib and Rosmah. Words after words, stories after stories, cartoon after cartoon, movie after movie, in the end history will do justice with words.

Najib and Rosmah you are responsible for the downfall of UMNO Baru, not the founder Mahathir. As a Malaysian with dignity and common sense, I do not see the reason why you need to hold on tightly to a party that was never yours in the first place. Mahathir allowed you to be a member and Chief of his party, you and Rosmah never applied to be a member. Yet you have the cheek to insult and be rude to the founder. It does not matter that Mahathir has left the party. History remain the same, Mahathir formed UMNO Baru in 13th February 1988. Today Mahathir can destroy UMNO Baru not you or any Sultan or your father’s spirit can stop that. But is Mahathir destroying his baby?

The one who is destroying UMNO Baru is YOU. You and Rosmah are the greediest bastards in the whole world. You destroyed your father’s legacy. You destroyed your own family by teaching your children and family members to be thieves. You teach the people to hate Islam and the Malay race by destroying and teaching the Judiciary, Parliament Speakers, Ministers MACC, PDRM, Armed Forces, AG, Government Servants and Sultans to be thieves and murderers.

Najib and Rosmah, both deserve to be punished not in cement drum but similar fashion as Teoh Beng Hock and Kugan.

Malaysians should learn never to let a person brought up with a silver spoon to lead this nation every again.

Karma has taught Mahathir a bitter lesson and let us Malaysians be united as one to teach Najib and Rosmah what crime can do to them.

The ERA of M.A.H.A.T.H.I.R is here.

What excuse will ROS Bitch ditch out?

UTM fucked big time

IF OPPOSITION PARTIES WERE TO WRITE SUCH MEMO, FIRE FROM RED HELL WILL POUR.

Which is worst – Ungrateful or Rude?

Rosmah Mansor took a stroll down memory lane this afternoon, recalling how she had known PKR vice-president Nurul Izzah when the latter was still a child with no teeth.

The wife of caretaker prime minister Najib Abdul Razak said she felt upset when the 37-year-old lawmaker addresses her by name, instead of her honorific title Datin Seri, aunty or makcik.

Dear All, what do you think when a person who was brought up by a father single-handed, refused to attend his funeral?

What do you think of a woman who refused to allowed her own mother to stay together with her biological father?

What is wrong when a person addresses another by the person’s name?

No need to get upset over a petty issue, when one does not have the dignity to hold a title or position.

A Brilliant Deal For Axiata, Celcom and PUC – Malaysia’s Largest Listed Internet Commerce Entity

Next week on 26th April, PUC will be holding its EGM to approve the acquisition of a 33% stake in Pictureworks, which comes with guaranteed profits for two years. PUC sprang a surprise just prior to the important EGM by disclosing the deal with 11th Street. In one fell swoop, we basically have the largest listed internet commerce entity in Malaysia.

Can anybody say that internet commerce will not grow even more significantly in Malaysia over the next 2, 5, 10 years? Well, how can anyone “participate” in that growth in a listed vehicle? Now you have it.

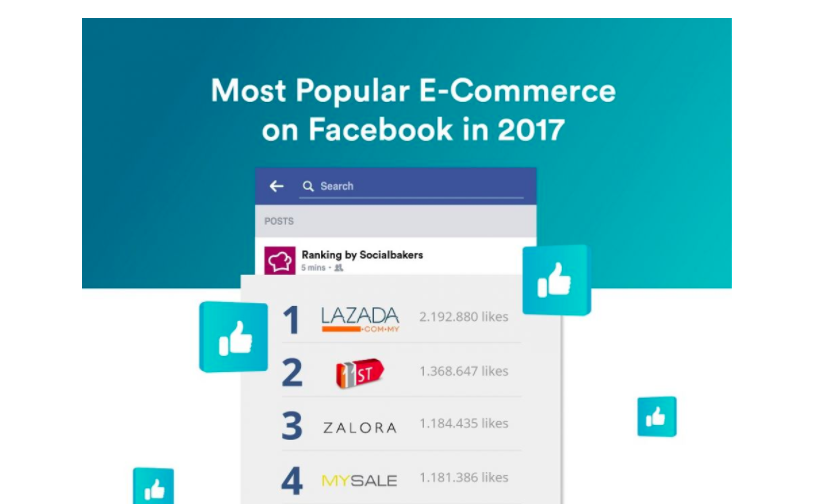

Ask yourself, can you buy a stake in Lazada or Shopee or even Zalora??? Yes, maybe when they actually list. Plus when they do, you can be sure the valuations will be astronomical (in the billions of USD).

Lazada, is backed by Ant Financial and Alibaba. Enough said.

Shopee is backed by Garena Group. Garena is backed by Tencent.

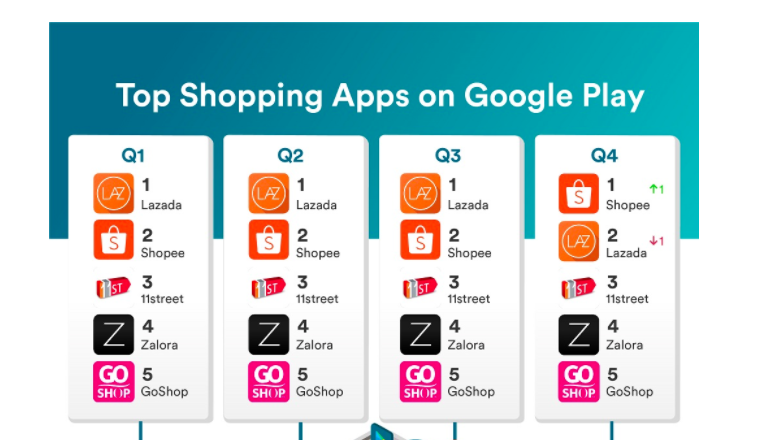

Celcom Planet Sdn Bhd is a joint venture between ADS and SKP, which owns and operates an e-commerce platform known as 11Street Malaysia, and is one of the largest e-commerce companies established in Malaysia. 11Street Malaysia was originally a leading e-commerce company in South Korea, operating under the management of SK Planet Co., Ltd. which expanded its operations to Malaysia to grow and expand the e-commerce industry in the country. From 2015 to 2017, 11Street Malaysia reported an achievement of more than 300% growth in gross merchandising value (“GMV”), 160% growth to over 13 million product listings, and 200% increase to 40,000 sellers registered on its platform. As of 31 December 2017, 11Street Malaysia recorded a GMV of approximately RM427million for financial ended 31 December 2017, and total monthly unique visitors (“UV”) of 13.5million for the month of December 2017.

The Investment Amount translates to an implied valuation of 100% equity interest in CPSB ranging from MYR333.33 million to MYR375.00 million (the “Implied Valuation”).

How expensive was the deal? If you were to take the historical Gross Merchandising Value of RM450m, it means PUC is coming in at a staggeringly cheap P/GMV of 0.6x. How cheap is that? Well, similar deals in the same tech sector have been in the 1.5-2.0x.

Why would Axiata/Celcom do such a deal? One, that the management of PUC has the ability and vision to take 11th Street to the next level. If you look at the new ownership structure, the original shareholders will still hold much hight stakes than PUC in 11th Street, so nobody’s cashing out.

I believe some of the RM90m will be used to pay down debt at 11th Street. The burn rate at 11th Street has passed the initial setup stage. They are recording good growth and good revenues, hence any synergies and cost savings will go swiftly to the bottom line.

PUC shall be appointed as a preferred partner of 11Street Malaysia provided that it shall offer competitive terms to 11Street Malaysia for the following (“Synergistic Collaboration”):- a. 11Street Malaysia’s marketing needs, especially in digital marketing; b. 11Street Malaysia’s payment gateway requirements for all its eCommerce services with PUC’s flagship digital services platform (“Presto”) being nominated and implemented as the Company’s preferred payment platform on all of its eCommerce services; and c. 11Street Malaysia’s technology needs for its eCommerce infrastructure and platform.

This is key to the transaction, elevation of PUC as the management and preferred partner. Obvious immediate synergies in e-marketing and e-advertising, the usual rice bowls for PUC. The management of PUC will be directing and putting in place the future direction of 11th Street, which is critical in being part of a listed entity.

PUC wishes to announce that the Company had on 12 April 2018 incorporated a wholly-owned subsidiary in Malaysia, namely PUC Ventures Sdn Bhd (“PVSB”), under the Malaysian Companies Act 2016 (“Incorporation”). PVSB is incorporated as an investment holding with an initial issued share capital of RM1.00 comprising one (1) ordinary share. It is intended that PVSB identifies opportunities to invest or acquire equity interests in and/or enter into strategic alliances / joint-ventures with companies which are principally involved in electronic commerce (“e-Commerce”) businesses, electronic payment services, financial services, technological services, and related businesses including but not limited to media services, airline and accommodation services related (“Target Segments”), which are synergistic and complementary to the existing businesses of PUC and its subsidiaries.

This announcement which came last week would actually be quite significant. The establishment of PUC Ventures would indicate that Pictureworks and 11th Street and e-Wallet and Presto etc… would not be just a mish mash of investments by PUC. It speaks of a bigger cohesive agenda by PUC going forward. I believe PUC is mapping itself as a smaller Meituan or Tencent.

CONCLUSION

a) Valuation wise – PUC looks particularly compelling – just taking into account the impending absorption of the proposed stake in Pictureworks, which is very undemanding. Added to the guaranteed profit for two years, Pictureworks has a very good chance to be listed in HKSE Gem, which will translate to a substantive “potential value unlocking” if/when Pictureworks lists. Just follow the steady roster of clientele of Pictureworks: Malaysia, HK, China, Singapore… but largely in China, which bodes well for a China/HK listing (comfort level based on source/location of revenues).

b) Valuation wise – As indicated above, the P/GMV for the 11th Street deal makes a lot of sense for PUC. Should they be able to bring up the revenues of 11th Street from 2017’s RM427m to a billion ringgit within 2-4 years, that would certainly make it highly attractive to list or be sold to even bigger whales at a valuation closer to 2.0x P/GMV. As always, 11th Street is a highly sought after asset platform, hence the permutations for a sale or joint venture or seperate listing are always on the table. Another potential kicker in PUC’s inherent value, which they bought at a very reasonable valuation.

c) A COUP – If you were to believe the media, JD.com and Alibaba were also trying hard to buy 11th Street. Of course both have bigger firepower and money, but then it would immediately lose its Malaysian roots. I think thats part of the broader strategy by Axiata/Celcom, to bring in a local champion and bring about much higher valuation, maybe a Malaysian “unicorn” in the making.

https://www.lowyat.net/2017/143327/report-alibaba-jd-com-competing-acquire-11street-malaysia/

d) Institutional Funds – Fund managers now can no longer ignore PUC. It is a “must have” being the biggest listed internet commerce entity. That should see an upsurge in institutional holders.

e) Data Science & A.I. – The bigger picture going forward. I think PUC is one of the very very few tech based companies that understand the whole ecosystem of the new world and the new future. PUC Ventures would be the vehicle to jumpstart alliances and investments. Just gauging its corporate moves for the past years and a half would paint a company and leadership that understands the really “big picture”.

My Forked Opinion

I am never surprise by the action and words of any Royal Household simply because I HAVE NEVER SEEN OR HEARD OF SITTING ROYALTY BEING POOR OR HAVE GIVEN THEIR WEALTH TO ITS OWN PEOPLE.

Have you?

63 years of living and day by day I can see for myself how these French fry are being brought up and lived. People who have never worked or suffered from not having any food to eat or have a bath or place to sleep are no ordinary human beings. These people are not living beings, in plain English these are lucky bums that God has forgotten he had created.

People like that are not in my list as Human Beings.

So what if one can squeeze projects worth billion ringgit for free.

So what if one owns hundreds of vehicles.

So what if one has a private army and hundreds of bodyguards.

So what if one has a jet, yacht, mansion overseas etc.

When majority of the Rakyat go to neighbour country to earn a living because in their own state there is no opportunity to earn a decent living, it is sorrowful.

When majority of the Rakyat are in the poverty range it is sorrowful.

When majority of the Malay Rakyat are into drugs it is sorrowful.

When majority of the Rakyat cannot read and write it is sorrowful.

Many assets of the state are been sold or given to foreigners it is sorrowful.

When majority of the Rakyat are not prepare for the future it is sorrowful.

When religious freak continues to impose stupid actions against the Rakyat it is sorrowful.

If I am a Royalty I will build a school to develop mind to strengthen the state development so that my own people do not have to travel far to earn a living. In other word, I will make sure my own people work in their own state and remain loyal to me.

If I am a Royalty I will stop corruption at all cost and execute such bastards.

If I am a Royalty I will bash the head of police, MACC, Judges and prosecutors for playing politic.

If I am a Royalty I will build a modern hospital free for my Rakyat.

If I am a Royalty I will make sure the people are not divided by race and religion instead be united.

If I am a Royalty I will build common place of worship.

If I am a Royalty I will make sure the people follow the law of the country and not politicians’ law.

If I am a Royalty I will never go into business or make money from selling titles and instead focus on being a silent guardian for the people.

SINCE GOD ALREADY KNOWS MY PLAN,

GOD THINKS BEING HUMAN BEING IS THE RIGHT GIFT FOR ME.