Since I have nothing bullish or non-depressing to post, I shall post about my all time fav albums. When we were younger, the list would change every few months, but the list kinda stop when you turn 35. See if you

have similar taste in music, or else you can post your fav in the comments section and reasons why. A better headline would be the top albums that I would take with me if I was LOST on an island with a CD player. While redoing the list, I found that I could not keep it to ten, it had to be twelve, hence Countdown from number twelve:

12)Tanto Tempo by Bebel Gilberto – Daughter of the brilliant Joao Gilberto. This is Brazilian music jazzed up and highly seductive and hypnotic. Best album from Latin America for the last 10 years, if not longer.

11) Tapestry by Carole King – If I did not have balls, this would have easily rated higher. So many songs from this album became timeless classics, such as You’ve Got A Friend and Will You Still Love Me Tomorrow. Its a great snapshot of a singer-songwriter right at the very peak of musical genius.

10) The Grand Illusion by The Styx – Loud, commercial but melodic band with loud hairstyles. Their best album by far. Every song has its own merits and weaved into a proper album. Derided by many but this album can stand the test of time. Check out The 70s Show parody of The Styx.

9)December by George Winston – Takes a lot to listen to one fella playing one piano with no additional instrumentation. Feeling wistful, philosophical, or just a quiet night to reflect. His notes lift you up and touches your soul literally. The title track, though instrumental may make your tears well up. Really.

8)Winelight by Grover Washington Jr & Bill Withers – Best romantic jazz ever. Enough said.

7)Silk Degrees by Boz Scaggs – This man has a weakish voice but his songs were brilliant. Again, this album captures him at his musical genius peak. Songs like We Are All Alone, Harbour Lights and my favourite Love Look What You’ve Done To Me. Highly under-rated.

6)Bat Out of Hell by Meatloaf – Another album that needed to be heard in its entirety. May be too melodic and commercial to rock fans but its the anthem 70s album for good reasons. Songs like Heaven Can Wait, Two out of Three Ain’t Bad and the title track – how not to be a top favourite.

5)Night At The Opera by Queen – Considered by many to be Queen’s best album, but not to me, its the second best.

4)Rumours by Fleetwood Mac – Too much grass and alcohol can turn out really good music. This dysfunctional group at its best. Every song is a gem. This album is one of the reasons why the 60s and 70s were considered to be the best periods for popular music.

3)How Dare You by 10cc – Not many would select this album but its pure genius. You have to listen more than a few times to love it and then you are hooked for life. Its whimsical, very melodic and adventurous.

2)Year of The Cat by Al Stewart – Absolutely fantastic folk rock album by an Englishman, very under-rated.

1)Sheer Heart Attack by Queen – This will always be my top album. Its their raw talent at their finest. If you have a relative 35 and above buy him this for Christmas, if its an over 35 lady, cannot go wrong with Winelight or December.

Missing Out

That’s the trouble with compilation lists. You feel bad that you left out a few which maybe deserve a place as your favourites. Here is a list of those albums that just missed out:

16 Lovers Lane by The Go-Betweens

A New World Record by ELO

Soul Deep by Jimmy Barnes

The Nightfly by Donald Fagen

Hotel California by The Eagles

Surfing With The Alien by Joe Satriani

Very Best Roll Over by Chage & Aska

A Decade of Steely Dan by Steely Dan

Btw, aren’t those album covers wonderful art pieces, certainly stood the test of time.

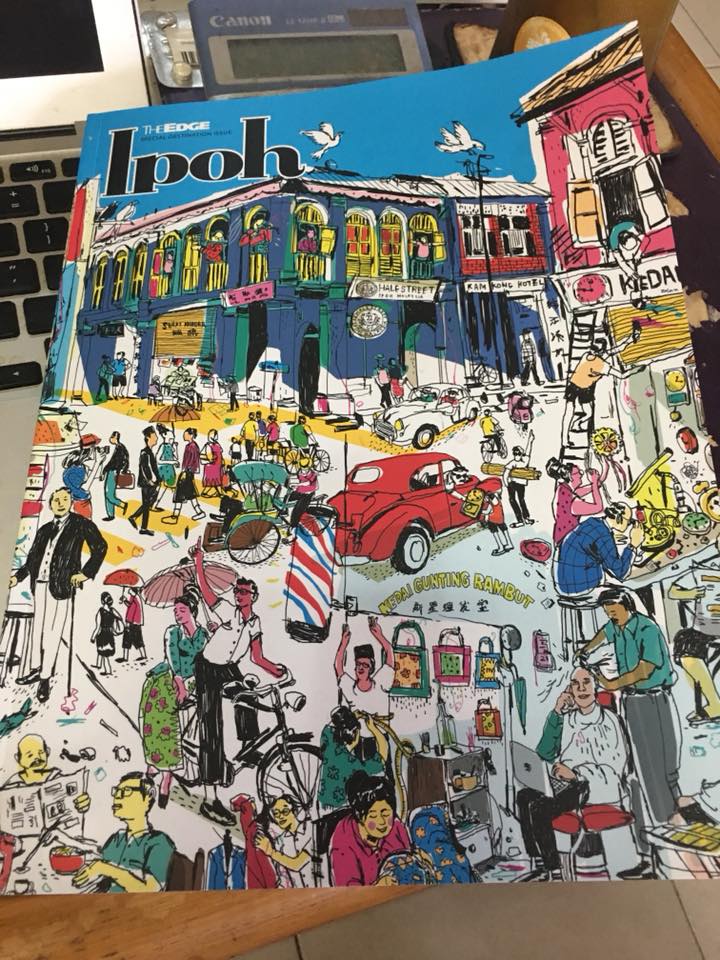

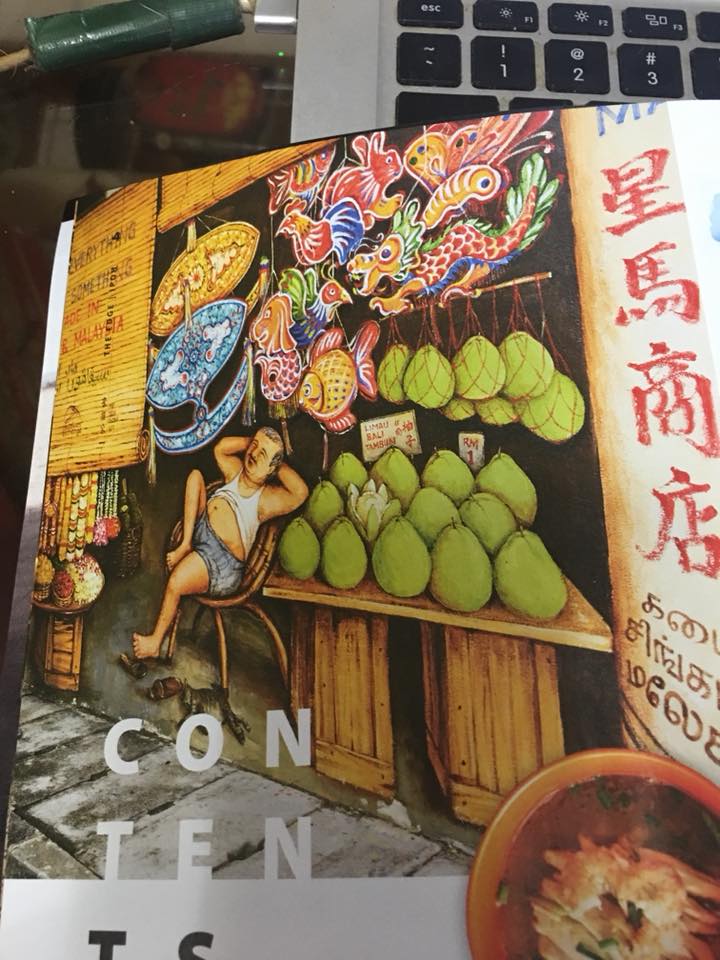

This weekend’s The Edge has a special destination guide to almost all n sundry in Ipoh. The lavish and ambitious 112 pager was read with much skepticism by yours truly.

But as an out and out Ipoh person, the publication is the best I have seen as a travel guide. There are plenty of nuanced references n insights that only the locals would know. The art works were spectacular n nostalgic. Photos the same.

Too important not to buy and keep.

This piece of artwork was so good in the details.

The watercolour depictions of Blue Mosque, HoYanHor bldg and Concubine Lane were exceptional.

Unfortunately, there was one mistake, a pretty big mistake … they put Cowan Street ayam tauge shop under “kaiseehorfun”.

Once and for all, kshf is made using prawn head stock as soup, has prawn slices, chicken, horfun/meen and kauchoy.

Ngachoykai has ngachoy and chicken with soy mix. You can have ngachoykai with any kind of noodles of rice even.

Below, a delectable snap of most of the popular Ipoh Chinese pastry snacks. Heartwarming and authetic.

I mean, if you are going to be an analyst, fund manager, private banker, sales trader of calibre .. take a stand. Make value-add comments and stand by them. There are too many humdrum, me-too, l”et’s all amble along so that nobody knows how average I am” mentality.

This has been well documented. The RM1.37bn purchase by Top Glove was completed only on April 4th this year. Secondly, the purchase was completed within 4 months.

There were glaring questions still not covered by the journalists.

Who were the advisors for Top Glove?

What actually did they advised?

Who did the due diligence?

Was it a limited due diligence, if so, there should be clawback, e.g. staggered payments till full due diligence is done.

Why was full sum paid prior to a full due diligence?

Was it too rushed?

If so, why the rush?

Where was the board’s view in the scheme of things?

Were the advisors well versed with billion ringgit acquisitions?

Where was the due diligence?

Who were the accountants for the private company beforehand?

How did they not qualify the financials before?

Malaysians are no longer stupid.

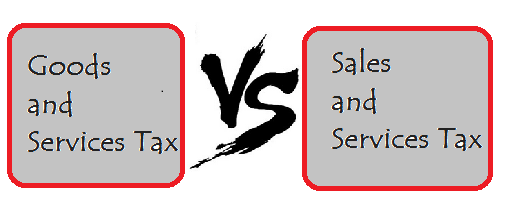

I believe it is time Malaysians should be given the right to a proper hearing before the implementation of SST.

Malaysians cannot continue to be ignored.

We voted for a better governing and we expect it.

From a collection of RM40 billion per year taxes to RM21 billion per year expected is not only unbelievable but no logic to it.

How then will the government find the balance RM19 billion to service the country?

Also under SST, cronies like Vincent Tan etc pays only 30% of their profit for taxation.

Malays, Indonesian and Bangla business will not pay a single sen tax.

So only a minority of the working class pay their due taxes.

Why must the minority take the burden?

How many more times does Anwar need to be stabbed?

Trust is not a worthy word given that family and close friends play each other out for financial gain or for power etc.

Everybody encounter it once or couple of times in their life.

But Anwar has the worst encounter not once but twice.

And the person who helped make this happens is Azmin.

Azmin has always being grateful to Mahathir for giving financial assistance to study, work and now a beautiful standing as Minister in Economic which he knows nuts.

So with the backing of Mahathir and Daim with fund of US16.91 billion which was stolen and transferred out of Malaysia recently what has Azmin Ali got to lose.

Win or lose, Mahathir is still the PM and his position as Minister is secure while the money is there to swim in.

AZMIN ALI IS DEFINITELY GOING TO CHALLENGE DSAI FOR THE TOP POST IN PKR.

Within 100 days already there are two death.

Encik Shahril of Sapura Energy had to defend his total take-home package of around RM70m a year for the past few years. Specifically since FY 2014.

His defense was that there was a covenant. If he won’t sell his shares, the company would get better interest rates on loans. Seemingly to imply that some major lenders will only lend to Sapura Energy only if he stayed.

Errr, that’s not the way a share market works. The remuneration committee cannot and should not take into account whatever “covenant” with lenders intimated with the CEO. It is like saying I am the CEO and I had to sell my mother’s house so that I don’t have to sell my shares in the company, so that share price doesn’t collapse and the lenders only wanted to deal with me as CEO. That’s not the way a share market works… I think.

Are you telling me that all 1,000 banks in Asia would not lend to you unless you stay as CEO and do not sell your shares? Even if that was the case, was the RM50-80m a year from FY2014 to compensate you for “opportunity cost” and “losses”? Who compensates the minority shareholders’ losses???? That’s not the way sharemarket works.

The remuneration committee can choose to reward the CEO if there had been reasonable stretch targets met, or even positioning the company to meet future challenges. The bottom line is that whatever you reward the CEO must have been to the benefit of ALL SHAREHOLDERS, either in new earnings achieved or price appreciation. There has been none of that.

You can try to argue that the CEO has positioned the company to face the new market conditions and restrategize the company’s direction over the last few years. Hence all shareholders will benefit from that. Again, while that is all good, IT MUST BE REFLECTED IN EARNINGS and PRICE APPRECIATION. If the positioning is so good for long term, then give la bonus WHEN these long-term strategies pan out. NOT BEFORE THAT.

The market cap of Sapura Energy has been between RM3.3bn to RM4.5bn over the last 12 months. At RM80m a year, that means the CEO gets approximately 1% to 2% of total market cap of the company a year. If the company continues to lose money, or even break even for 10 years… it means the CEO would have gotten between 10% to 20% of the market cap of the company for not doing terribly well.

Mind you Encik Shahril owns just 16%, which translates to a value of RM520m to RM720m. Now put that in perspective, RM70m-RM80m in compensation a year is a bit much.

That’s certainly not how the share market works. I think.

(above is a copy of the remuneration framework of a good listed company … in this case, it was Apple Inc.)

It is not just at Sapura Energy. Just go and examine the total board compensation, in particular to the CEO, of the following companies. The board remuneration is totally out of whack with whatever business metrics you want to use to measure good or great performance:

Genting

KNM

Salcon

Maybank

IHH Healthcare

IOI

Maxis

TA Enterprise

YTL

There are those who are owner controlled, which makes it difficult when they pay themselves an over the top amount. You already owned a controlling stake, if you perform well, your equity will rise. Be like Li Ka Shing, he pays himself HK5,000 dollar a year as compensation.