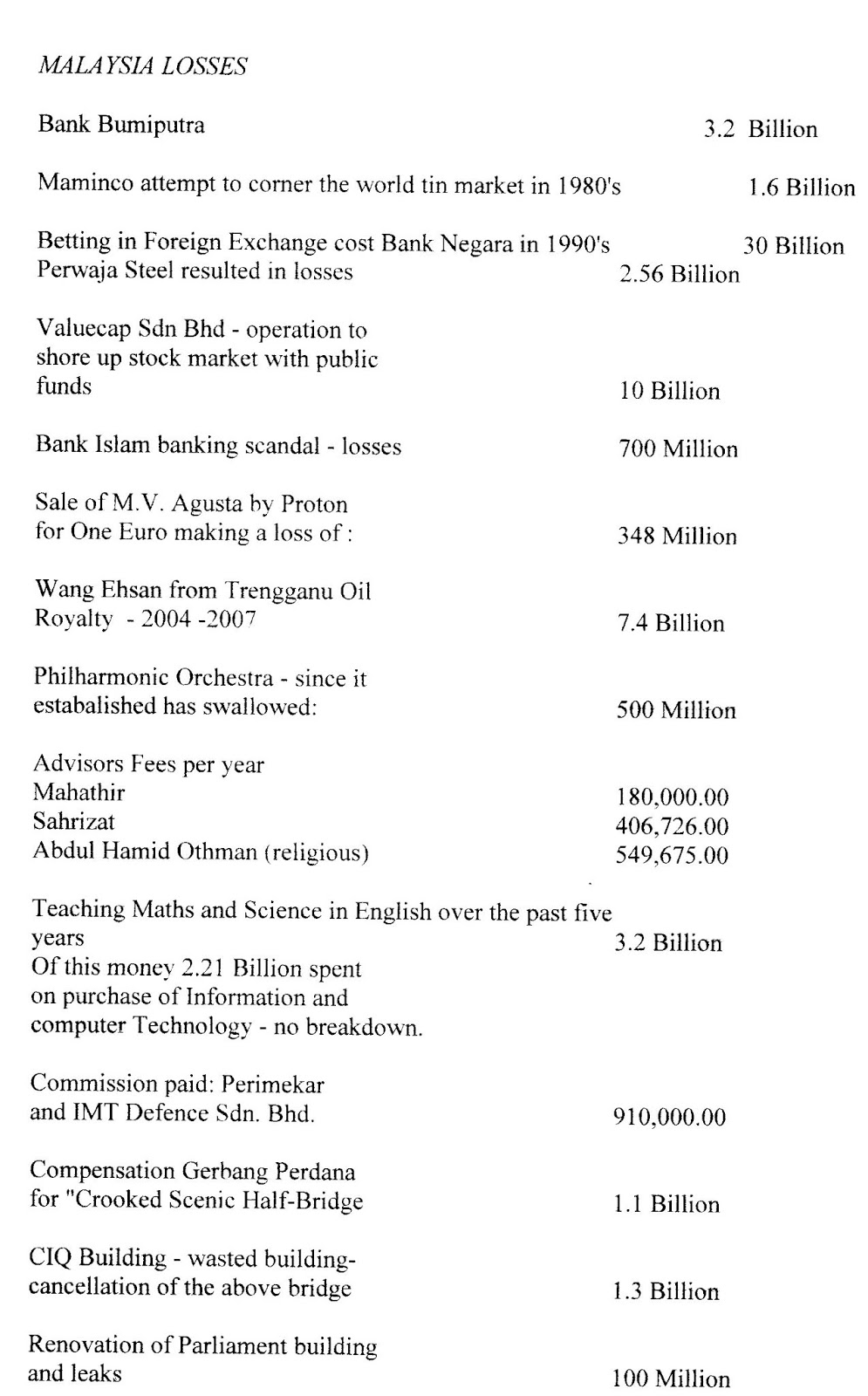

LOSSES FROM 16TH JULY 1981 TO 31ST OCTOBER 2003

LOSSES FROM 10TH MAY 2018 TILL 9TH FEBRUARY 2020 MALAYSIA SUFFERS LOSS OF RM100 BILLION.

SO WHAT IS GOOD ABOUT MAHATHIR?

LOSSES FROM 10TH MAY 2018 TILL 9TH FEBRUARY 2020 MALAYSIA SUFFERS LOSS OF RM100 BILLION.

SO WHAT IS GOOD ABOUT MAHATHIR?

Here is some very high level arithmetic by Lim Guan Eng :

The 18% saves the people and govt RM42bil to RM43bil

My comments : Let us use a real live example and do some arithmetic.

Everyday for 6 days a week my wife and I pay a minimum RM10.60 toll to Plus to get to work and back.

That’s RM63.60 a week.

Lets keep it simple and multiply by four weeks, round it up, and get RM255.00 per month.

So for one year I pay RM3,060.00 to Plus just to drive to work and back.

This means for the remaining 18 years until 2038 I will pay Plus = RM55,080.00

Now Guan Eng says I get an 18% discount.

But Guan Eng has extended the toll by another 20 years which becomes 38 years.

So lets take (1 year’s toll minus 18% x 38 years) :

(RM3,060.00 – 18%) x 38 yrs = RM95,349.60 !!

So my choice is between

i. paying a total RM55,080.00 over the next 18 years (the No Changes Option)

ii. paying a total RM95,349.60 over the next 38 years !! (with 18% discount)

I am actually paying Plus 94% MORE TOLL over 38 years !!

Guan Eng certainly will have used the Net Present Value method to discount the future cashflows of Plus.

But the ordinary citizen with a wife, three kids, car and housing instalments to pay does not do any Net Present Value calculations when he stops at the Toll Gate. It is simply got money or no money in the pocket.

But Guan Eng’s arithmetic says :

The Edge:

The Singapore exchange is about to make life easier for listed companies — the safer ones, at least.

The bourse’s regulatory arm plans to end quarterly earnings reporting requirements that currently apply to all companies with a market capitalization of at least S$75 million ($56 million), according to Tan Boon Gin, the chief executive officer of Singapore Exchange Regulation.

When the rule change takes effect on Feb. 7, only riskier companies will need to report earnings every three months, Tan said at a press briefing. SGX RegCo will also tighten other disclosure rules and introduce a new whistleblowing policy as part of efforts to protect investors, Tan added.

Additional disclosure requirements will be introduced for rights issues

Acquisitions that reduce net profit or net asset value by 20% or more, or where the target is loss-making or in a net liability position, will be subject to listing rules.

Companies will need to appoint an independent valuer for significant asset disposals.

Firms will be asked to disclose material price- and trade-sensitive information, and any changes to near-term earnings prospects.

(Sept 19): AirAsia Group Bhd chief executive officer Tan Sri Tony Fernandes said he agrees with US President Donald Trump’s call for companies to issue financial reports just twice a year, rather than four times, as it drives analysts to make short-term decisions.

“One of the few things I agree with Donald Trump is quarterly reporting is null and void. Should be six months. Analysts driving to much short-term decision,” he said via Twitter today.

My View:

a) QR should stay. Any listed company, big or small, should have the discipline of being able to look at their financial status at ANY TIME, be it monthly or quarterly at the bare minimum. Half-yearly leaves too much room for things to happen. A company’s management should have the desire to be able to close their books at a week’s notice. Financial discipline is paramount to any company that rides on sound management and have a close eye on deviations. If a company needs to have that, investors should be just as eagle-eyed.

b) QR may be lighter in its requirements. Just the basic financials BS/CF/IS, plus commentary on substantive changes to Debtors and Creditors, or any revaluations/disposals of significance. Keep it to the bare minimum.

c) QR does not and should not add much financial burden on listed companies. As mentioned, all companies should be able to close their books within a week. Are you to tell me monthly meetings obtain figures for discussion that are 6 months past? These are things all listed companies should be doing already.

d) QR would also “help to reduce the leeway” for the massaging of earnings. Enough said.

e) There is already insufficient information pertaining to the company’s fundamentals. The sector’s prospects and outlook are not being highlighted sufficiently by basic financial media. Only the top 40 stocks in Malaysia get any form of decent analyst coverage, what about the other 900? There is a dearth of “credible information” for local investors on local stocks. If The Edge can find a willing audience on a daily basis, shouldn’t that tell you investors need better information flow?

f) Half-yearly reporting also gives rise to “insider knowledge”. The longer the reporting period, the higher the “value” that is accrued to insiders. Owners, board members, CFOs, accountants, corporate lawyers, industry followers, insider share movements, etc… all will benefit more from Half-Yearlies than QR.

g) If you were a substantive shareholder, would you be happy to only get a half-yearly update on your invested company? No. Why should normal investors be deprived of that information?

h) Does QR limits a company’s long range planning? No. Why should short term price gyrations affect your company if your fundamentals are strong. Eventually all QRs will even out positively if your long term fundamentals are good. Yes, stocks will react to QRs, but these are the norm of a market, a daily market place that tries to forward discount a company’s prospects.

If you argue for long term reporting, why not report all earnings in one month and then close the market for one year, then report again… that is as preposterous as eliminating QRs.